Sunnova: Short 0.25% Convertible Notes Due 2026

Short 0.25% Sunnova Energy International Inc. Convertible Unsecured Notes Due 2026 at 27.125/30.125 as of March 4, 2025

〰️

Short 0.25% Sunnova Energy International Inc. Convertible Unsecured Notes Due 2026 at 27.125/30.125 as of March 4, 2025 〰️

Situation Overview

Sunnova Energy International Inc. (NYSE: NOVA) has been burning cash since its inception dating back to its earliest publicly available financials for 2017. Sunnova’s consistent operational cash burn has been offset by its ability to raise capital through securitizations, tax equity funds, corporate debt and the equity markets. Favorable legislation and incentives during prior administrations have been key to the growth of Sunnova and its peers, attributable to Department of Energy guarantees, net energy metering programs, solar renewable energy credits, or SRECs, investment tax credits, or ITCs, among others.

While Sunnova claims to be a solar energy as a service, or EaaS, provider, at its core Sunnova is a solar energy system financing business where funds raised through securitizations, managed tax equity funds, corporate debt and common equity issuances are used to acquire solar energy systems and loan agreements originated through its network of dealers. These systems generate monthly cash revenue by providing energy to customers through power purchase agreements, or PPAs, and lease agreements, and from payments on customers’ loan agreements.

Sunnova is a spread business where its customer contract internal rate of return must exceed its cost of capital. The high-interest-rate environment over the past few years has severely pressured its spread, making it an unattractive business.

Coincidentally, in 2024, the sale of ITCs emerged as a major opportunistic tailwind for Sunnova and its peers’ cash generation. Chasing these ITC incentives, Sunnova increased its ITC rate on originations to the “low 40s [percentage range]” in the fourth quarter of 2024. Sunnova’s weighted average ITC rate in 2024 was 38.3%, compared with 31.5% in 2023. For a moment, ITC sales appeared to be Sunnova’s salvation, however, their cash generative prowess quickly diminished with the new Trump administration. Now the future of ITCs is very bleak.

During the fourth-quarter earnings call, CEO John Berger painted a picture of a cautionary consumer and capital provider environment exacerbated by post-SunPower bankruptcy market concerns, the unclear future of the Inflation Reduction Act of 2022 and other legislative incentives and a high-interest-rate environment. This backdrop, coupled with subdued solar market growth expectations for 2025, limited Sunnova’s access to capital, which would have otherwise been deployed to generate operational CF, over the past few months. Amplified risk surrounding the business has exponentially increased Sunnova’s cost of capital, illustrated by its recent secured KKR term loan priced at 15%, in turn shrinking its spread.

Nearly all customer contracts that Sunnova originates are held in subsidiaries that are variable interest entities, or VIEs, which are financed through securitizations or tax equity funds and equity contributions from Sunnova. Sunnova reports its financials on a consolidated basis, combining the results from the VIEs with the results from its operations. However, Sunnova’s $2 billion of corporate-level debt is structurally subordinate to $7.2 billion of securitization debt regarding the payment streams on its customer contracts. In other words, asset value within these securitization vehicles would first offset subsidiary-level debt with only any remaining equity value flowing to the corporate-level.

While it appears that Sunnova is able to service its securitization vehicles with cash flows from its customer contracts, the value of residual equity that flows to Sunnova’s corporate debt remains severely restricted. The lack of unrestricted cash generation out of its securitization vehicles up to the corporate level poses a significant threat of default on its corporate debt coming due in 2026 and 2028. Sunnova has $400 million of 5.875% unsecured notes due Sept. 1, 2026 and $575 million of 0.25% convertible unsecured notes due Dec. 1, 2026. Followed by $400 million of 11.75% unsecured notes due Oct. 1, 2028 and $600 million of 2.625% convertible unsecured notes due Feb. 15, 2028.

Investment Thesis

Candid Value estimates that corporate debt at Sunnova Energy Corporation would recover approximately 29.5%, while the convertible notes at Sunnova Energy International Inc. would recover 0% if Sunnova’s customer contracts are discounted at a more realistic rate of 13.5% to 15%, as opposed to the 6% rate utilized by the company. We believe the use of a discount rate higher than the company’s is warranted given the glaring economic uncertainty surrounding the business.

Candid Value uses a top-down approach based on discounting cash flows from the assets within the securitization vehicles in comparison with Sunnova’s total securitization debt, as opposed to valuing each equity tranche of the company’s multiple securitization vehicles individually. While this is an oversimplification, we believe this is representative of Sunnova’s equity value in these vehicles given the lack of publicly available information pertaining to these subsidiaries. Candid Value concludes that there is negligible residual equity value flowing out of Sunnova’s securitization vehicles to the corporate level.

Candid Value employs Excel’s “PMT” function to calculate estimated monthly net cash flows stemming from Sunnova’s customer contracts. The company provides “estimated gross contracted customer value” and “estimated gross renewal customer value” figures in its supplemental financials, while it discloses construction-in-progress amounts in its 10-Ks and 10-Qs. Candid Value spreads these monthly cash flow streams over the average remaining life of its contracts and discounts them back at a rate of 13.5% to 15%, which better aligns with Sunnova’s current cost of secured capital.

The Excel spreadsheet used to calculate Candid Value’s recovery estimates is available for download at the top of the page. Candid Value’s Sunnova waterfall analysis is shown below:

As of Dec. 31, 2024, estimated gross contracted customer value and estimated gross renewal customer value were $10.3 billion and $1.1 billion, respectively, at a 6% discount rate. Estimated gross contracted customer value represents the net present value of initial current customer contracts (including power purchase agreements, leases and loans), which currently have a weighted average remaining life of 19 years, according to the 10-K, while estimated gross renewal customer value represents the net present value of expected-to-be-renewed customer PPAs and lease contracts over a 10-year period (two five-year renewal terms) following its initial contract completion. Sunnova assumes that 100% of its PPA and lease agreements would be renewed for each five-year renewal period at a price 10% lower each period. Sunnova discounts all future cash flows at a 4%, 6% and 8% discount rate in its supplemental financials.

Construction-in-progress represents solar energy systems and energy storage systems that the company expects to be contracted under power purchase agreements or leases in the near future. Sunnova had $499 million of construction-in-progress within its property and equipment balance sheet line item as of Dec. 31, 2024. Candid Value assumes that Sunnova values these assets at a 6% discount rate, similar to that used for its other customer values. For simplicity, Candid Value assumes that all of these contracts would begin in June, allowing for six months of ramp time, and run for a total of 35 years, an initial contract period of 25 years plus two five-year renewal contract periods, consistent with Sunnova’s contract length and 100% renewal rate assumptions. However, this simplification does not account for the 10% price decrease during each renewal period.

Sunnova had $126.7 million of balance sheet inventory as of Dec. 31, 2024. Candid Value adds inventory to corporate-level distributable value at book value. It is possible that certain materials could be sold at higher prices if potential significant tariff hikes on solar panel cells from Cambodia, Malaysia, Thailand and Vietnam are implemented.

Sunnova warns that its estimated future cash flows “reflect the projected monthly customer payments over the life of [its] solar service agreements and depend on various factors including but not limited to solar service agreement type, contracted rates, expected sun hours and the projected production capacity of the solar equipment installed.” Without further disclosure as to these variables, it is difficult for Candid Value to estimate how changes to them might impact total contract value. For example, delinquency and cancellation rates could be expected to increase in times of economic uncertainty. Additionally, any tariffs implemented on solar panel cells or other equipment from overseas should cause embedded operations and maintenance expense assumptions to increase.

Sunnova’s estimated gross contracted customer value and estimated gross renewal customer value underlying assumptions are discussed in greater detail towards the end of the report.

Securitization Debt Principal Amount Increased to $7.2B as of March 2

Sunnova’s capital structure pro forma the issuance of the SOL IX asset-backed notes and the KKR term loan is shown below:

On Feb. 21, an indirect subsidiary of Sunnova entered into $282.3 million of 6.28% Series 2025-P1 Class A solar asset-backed notes and $13.5 million of 8.65% Series 2025-P1 Class B solar asset-backed notes with a maturity date of January 2060. The notes were issued at a discount of 4.59% for the Class A notes and 3.46% for the Class B notes. The notes are secured by, and payable from the cash flow generated by, the membership interests in the SOL IX issuer subsidiary’s wholly owned, direct subsidiaries and the sale of renewable energy credits.

Candid Value omits the SOL IX debt and potentially its corresponding asset values from this analysis, assuming there would be no excess equity value flowing out of the vehicle. It is unclear whether the contracts collateralizing the SOL IX facility were embedded within gross customer value or construction-in-progress as of Dec. 31, 2024, or whether these contracts were generated after year-end.

On March 2, Sunnova entered into a $185 million nonrecourse asset-based term loan due 2028 provided by KKR that bears interest at 15% per annum. This is included as nonrecourse subsidiary debt at $240.5 million, incorporating its required payback of at least 1.3x invested capital. We also include the corresponding cash proceeds of $175 million accounting for the original issue discount of $10 million as an addition to corporate-level distributable value.

Convertibles Notes Are Subordinated in Right of Payment

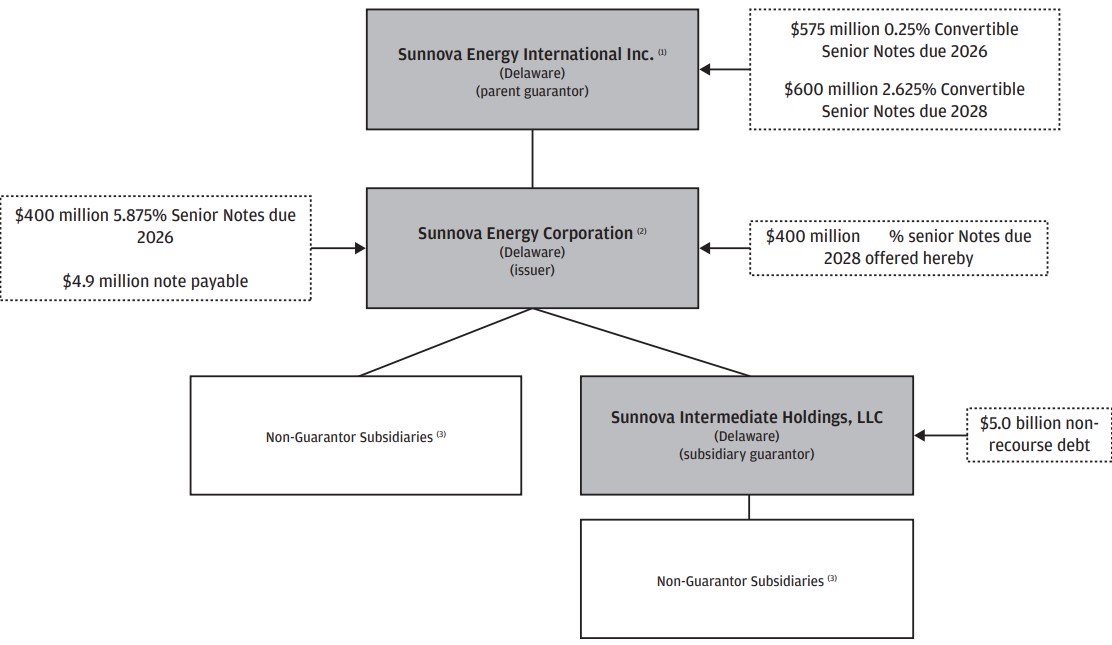

The two series of Sunnova Energy Corporation notes are guaranteed by Sunnova Energy International Inc. and Sunnova Intermediate Holdings LLC. The two series of Sunnova Energy International Inc. convertible notes do not contain any guarantees. As a result, the 0.25% convertible unsecured notes due 2026 and 2.625% convertible unsecured notes due 2028 are subordinated in right of payment with respect to the 5.875% unsecured notes due 2026 and 11.75% unsecured notes due 2028. A simplified organizational structure, included in the offering memorandum for its 11.75% unsecured notes due 2028, is shown below:

Not All of Sunnova’s Unrestricted Cash Is Equivalent

As of Dec. 31, 2024, Sunnova had total consolidated cash of $548.1 million. The company classified $336.9 million as restricted cash and $211.2 million as unrestricted cash. However, $176.5 million of its unrestricted cash balance serves as collateral for its nonrecourse financing arrangements held in collection accounts at its special-purpose entities that is available for distribution to Sunnova only after satisfying the current obligations of the applicable special-purpose entity each payment period.

Certain of these financing arrangements require all excess cash flows from the special-purpose entity to be used to repay the financings in full prior to distributing any cash flows to Sunnova, for which the residual equity interests in all its securitizations will be pledged as collateral. Although Sunnova classifies this cash as unrestricted, the company may be required to use it to pay down securitized debt before it flows up to the corporate debt.

Restricted cash represents cash held to service certain payments under Sunnova’s various financing arrangements, to be used to purchase eligible solar energy systems and balances collateralizing outstanding letters of credit related to a reinsurance agreement and one of its operating leases for office space, as shown below:

As a result, Candid Value estimates $434.4 million of subsidiary-level restricted cash that could be used to service its securitization before flowing to corporate debt, and $34.7 million of unrestricted cash at the corporate level. These amounts exclude $73.4 million of tax equity reserves restricted cash and $5.7 million of collateralized letter of credit and operating lease restricted cash.

Candid Value Forecasts Q1 2025 Cash Burn of $118M

Based on historical results, Candid Value estimates that Sunnova would burn $118.1 million of corporate-level cash in the first quarter of 2025. Candid Value excludes cash proceeds from the sale of ITCs in its calculation due to the uncertainty surrounding their usage. We assume the company has burned cash year-to-date at similar levels to 2024, which we believe captures the seasonality of the business. We calculate levered corporate-level CF for the first quarter of 2024 as follows:

It is important to decipher Sunnova’s cash flows at the corporate level versus the subsidiary level for the purpose of this analysis. As a result, Candid Value’s historical corporate-level cash flow calculations are disaggregated below. Candid Value aggregated various consolidated cash flow items to arrive at proxies for capital inflows and outflows.

Sunnova’s Values for Customer Contracts Incorporate Undisclosed Assumptions

Sunnova provides estimated gross contracted customer value and estimated gross renewal customer value in its supplemental financials on a quarterly basis, which can be used as a proxy for contract values as of a specific date in time.

Estimated Gross Contracted Customer Value

Estimated gross contracted customer value represents the following:

The sum of the present value of the remaining estimated future net cash flows Sunnova expects to receive from existing customers during the initial contract term of customer agreements, which are typically 25 years in length;

Plus the present value of future net cash flows Sunnova expects to receive from the sale of related SRECs, either under existing contracts or in future sales;

Plus the cash flows Sunnova expects to receive from energy services programs such as grid services; and

Plus the carrying value of outstanding customer loans on its balance sheet.

From these aggregate estimated initial cash flows, Sunnova subtracts the following:

The present value of estimated net cash distributions to redeemable noncontrolling interests and noncontrolling interests; and

Estimated operating, maintenance and administrative expenses associated with the solar service agreements.

The anticipated operating, maintenance and administrative expenses include, among other things, expenses related to accounting, reporting, audit, insurance, maintenance and repairs. In the aggregate, Sunnova estimates that these expenses are $20 per kilowatt per year initially, with 2% annual increases for inflation, and an additional $81 per year non-escalating expense included for energy storage systems. Sunnova does not include maintenance and repair costs for inverters and similar equipment, as those are largely covered by the applicable product and dealer warranties for the life of the product, but it does include additional cost for energy storage systems, which are covered by only a 10-year warranty.

Estimated Gross Renewal Customer Value

Estimated gross renewal customer value represents the sum of the present value of future net cash flows Sunnova would receive from customers during two five-year renewal terms of its leases and PPAs, plus the present value of future net cash flows Sunnova expects to receive from the sale of related SRECs, either under existing contracts or in future sales. From these aggregate estimated renewal cash flows Sunnova subtracts the present value of estimated net cash distributions to redeemable noncontrolling interests and noncontrolling interests and estimated operating, maintenance and administrative expenses associated with the solar service agreements.

Sunnova’s estimated renewal gross customer value uses “the established industry convention, which assumes 100% of solar leases and PPAs are renewed, due to the expected useful life of the system and costs to the customer associated with an election to purchase or remove the equipment.” The company further assumes that these contracts are renewed at 90% of the contractual price in effect at expiration of the term of the solar service agreement. Since the customer has two renewal options of five years each, for the second renewal period Sunnova assumes a contractual price of 90% of the price in the first renewal period. Loan agreements are not included in estimated renewal gross customer value, since they do not contain a renewal feature.