Jeld-Wen: Long 4.875% Notes Due 2027

Long 4.875% JELD Notes Due 2027 at ~80.25 as of May 13, 2026

〰️

Long 4.875% JELD Notes Due 2027 at ~80.25 as of May 13, 2026 〰️

Situation Overview

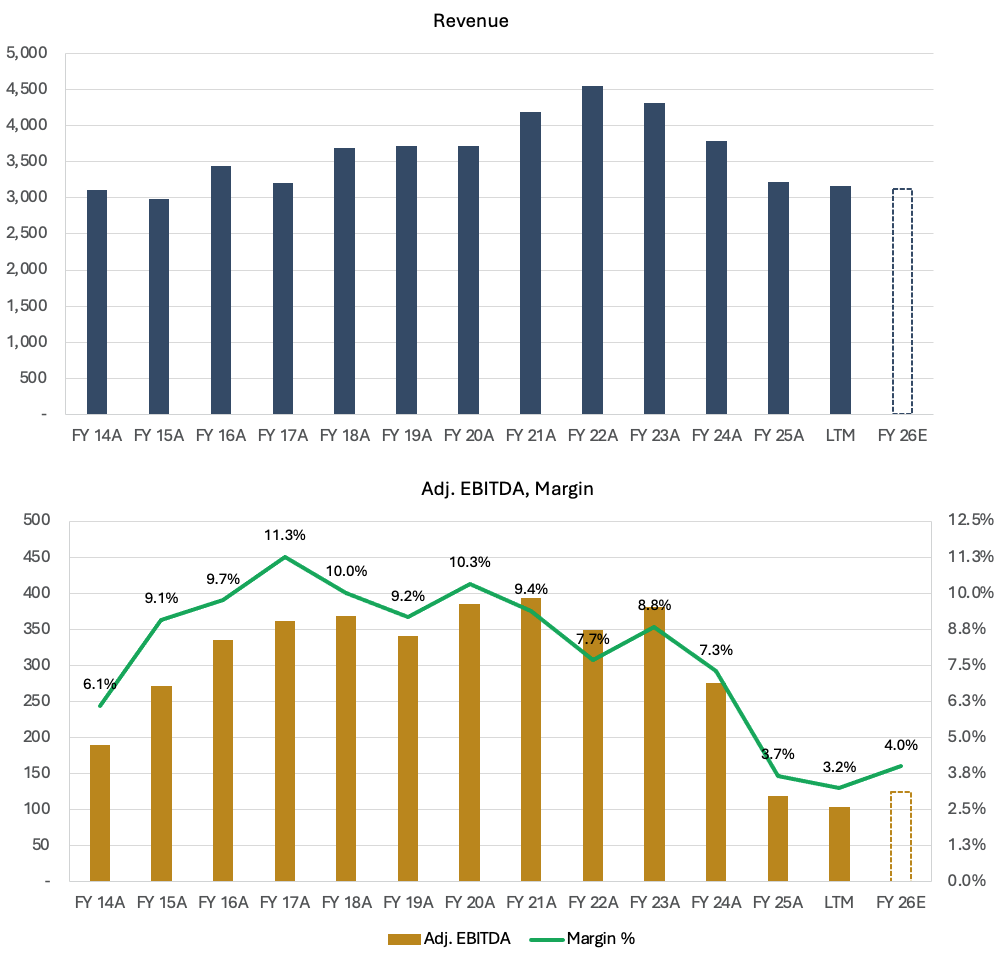

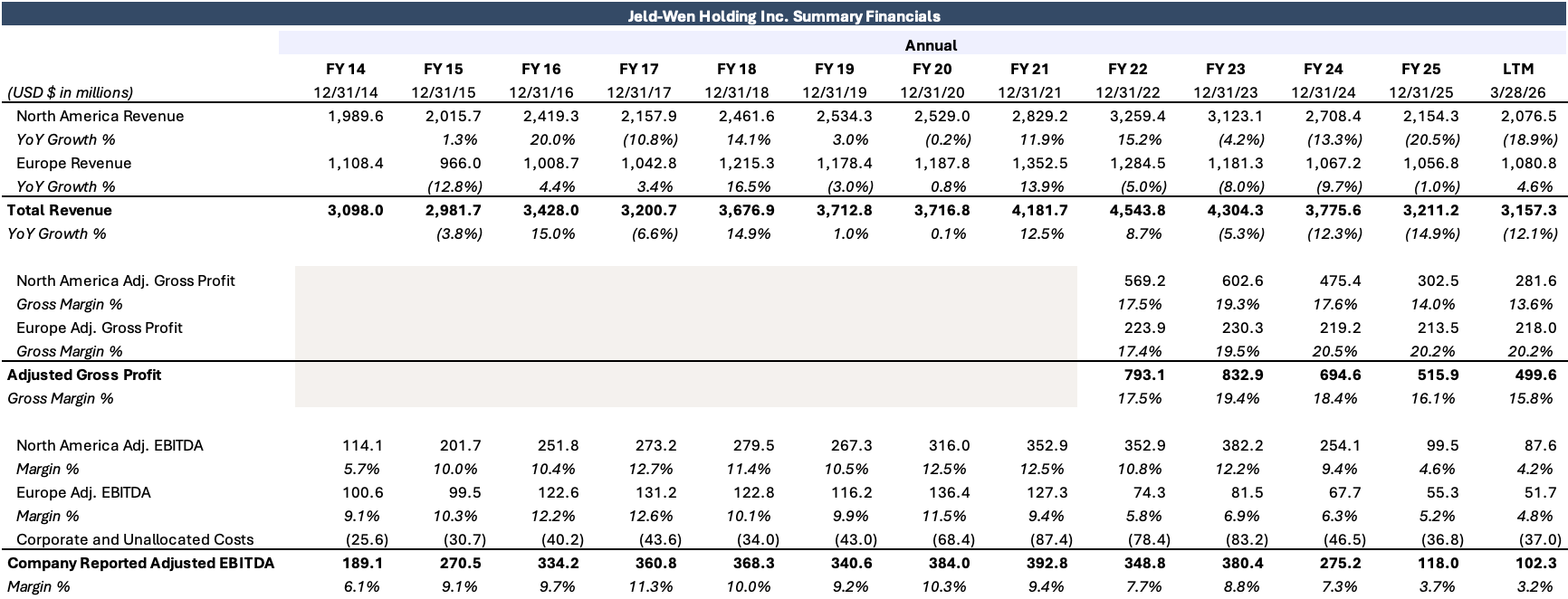

Windows and doors maker Jeld-Wen Holding Inc. (NYSE: JELD) is a classic example of a distressed situation— a cyclical manufacturer burdened by an over-levered balance sheet, experiencing bottom-of-the-cycle earnings with severely compressed margins and negative free cash flow, without prospects for a near-term top-line recovery. For the trailing-twelve-month period ended March 28, the company generated revenue of $3.157 billion and adjusted EBITDA of $102.3 million, a decline from its lowest reported annual adjusted EBITDA of $118 million and fourth-lowest annual revenue of $3.211 billion to date in 2025 (representing its North America and Europe segments, excluding its divested Australasia unit).

This is not the company’s first time in distressed territory as it nearly went bankrupt after the subprime mortgage crisis, before private equity firm Onex stepped in with an $871 million investment in 2011, including $700 million of convertible preferred stock and $171 million of convertible notes (which were all ultimately converted into common stock), used to address imminent debt maturities at the time.

Under Onex’s ownership, Jeld-Wen’s balance sheet continued to grow through an aggressive roll-up strategy followed by dividend recapitalizations, the quintessential PE playbook. Jeld-Wen has completed over 13 acquisitions since then and distributed over $800 million through dividend recaps. The company went public in January 2017. Onex began offloading its position as part of the IPO and completely exited predominantly through secondary offerings by August 2021. According to a case study published by Onex in 2021, which has since been removed from its website, the firm made approximately $2.4 billion on its Jeld-Wen investment when accounting for dividends, recapitalizations and other distributions.

Onex exited Jeld-Wen towards the top of the cycle with single-family new housing unit starts hitting pre-subprime mortgage crisis highs, and COVID-induced demand fueling the repair & remodel market. These tailwinds produced Jeld-Wen’s highest revenue years in 2022 and 2023, before the post-COVID housing boom faded and rising interest rates crushed new construction and R&R demand. At this time, it became apparent that Jeld-Wen’s capital structure was no longer sustainable at subdued market demand levels as a flurry of operating inefficiencies surfaced, further exacerbated by significant cost inflation.

Candid Value believes that Jeld-Wen is a highly cyclical, moderate-to-high operating leverage business that thrives under high market demand periods but plummets when its break-even volume threshold is not met.

According to Candid Value, the following factors have caused significant operating deterioration at Jeld-Wen: a fragmented and inefficient manufacturing and distributing network; unrealized synergies stemming from improper integration of acquisitions; the court-ordered divestiture of its higher-margin Towanda, Pa., door-skin business; significant input cost inflation, particularly in freight, materials and energy; continued new housing construction and R&R market weakness; sales volume deleverage; and market share loss.

Despite the current trough in Jeld-Wen’s end markets, Candid Value believes a rebound is inevitable. It’s more of a question of when, not if a recovery will occur. Candid Value believes that investors can position themselves to capture inevitable medium-term recovery upside while capping downside risk.

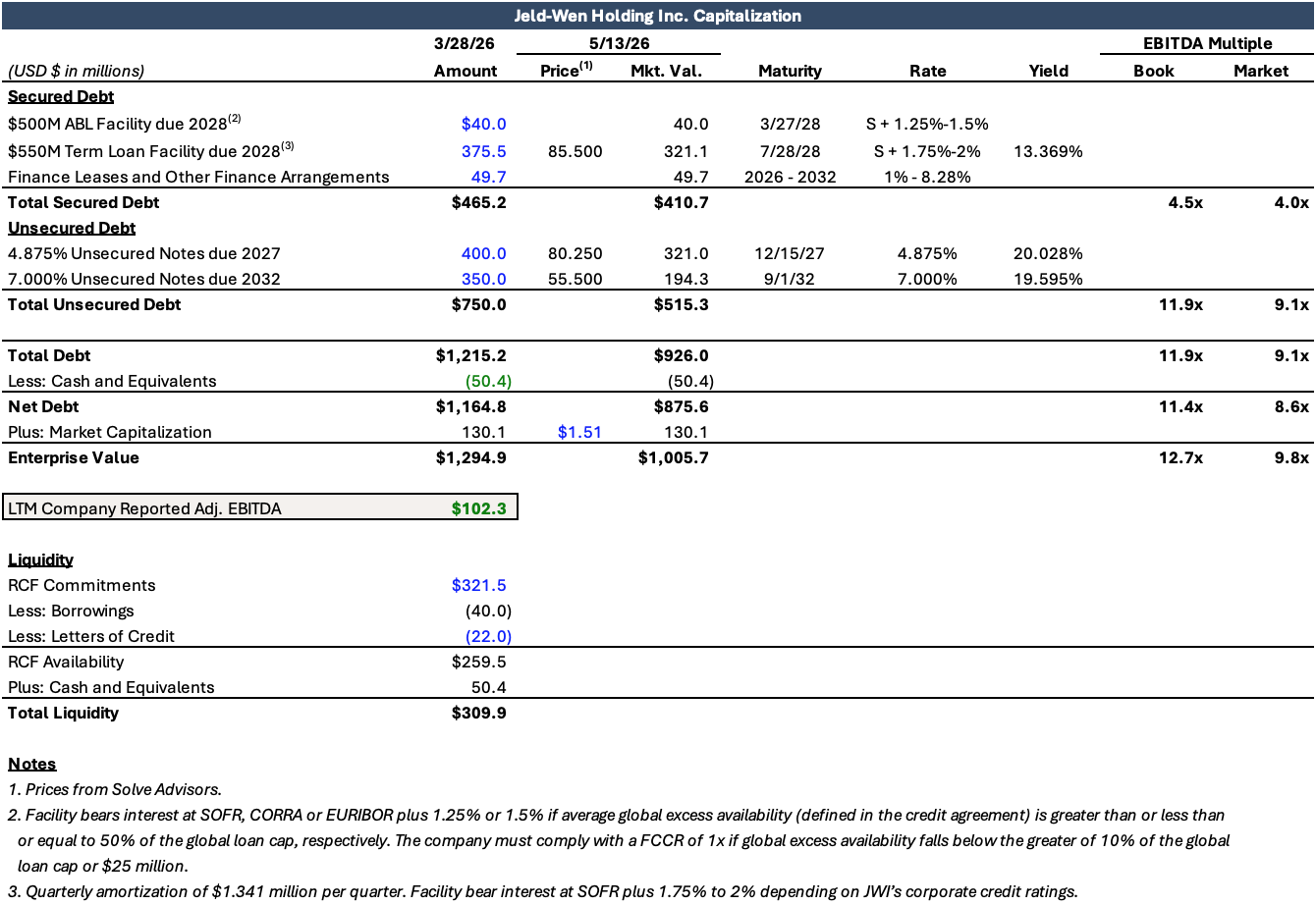

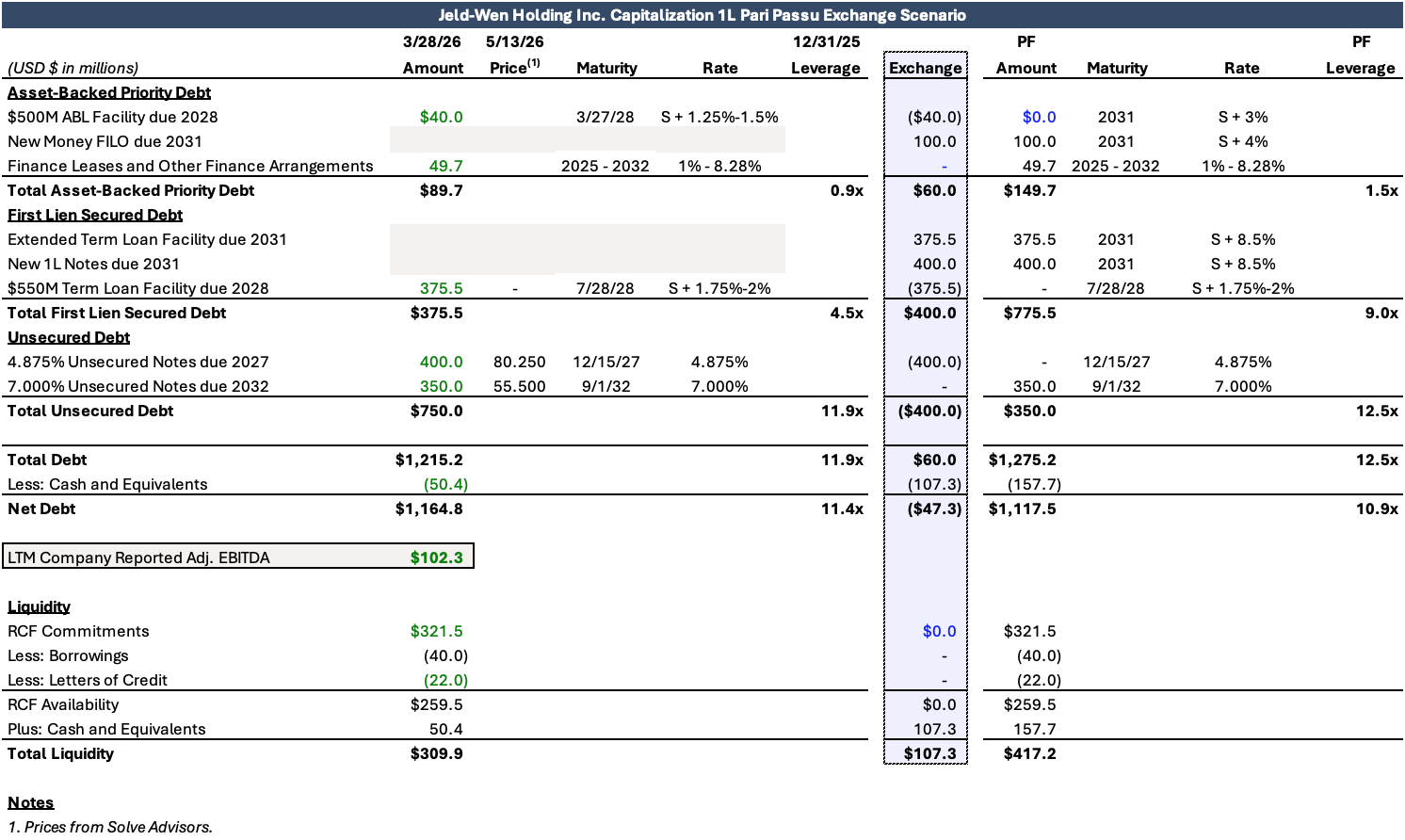

Jeld-Wen Holding Inc. has $400 million of 4.875% unsecured notes maturing on Dec. 15, 2027, followed closely by the maturity of its asset-backed revolving facility ($40 million drawn with $259.5 million available as of March 28) on March 27, 2028, and $375.5 million of term loans maturing on July 28, 2028.

The company’s credit documents are incredibly loose with substantial debt incurrence and restricted payment/investment capacities, along with no pro-rata sharing provision and no modern liability management exercise, or LME, protections. In our view, this provides the company flexibility to execute any flavor of LME it chooses.

Management’s primary objective in potential discussions with lenders is to extend its maturity wall and raise new money to offset expected free cash flow burn in 2026 of $70 million and beyond, tiding it over until a rebound within its end markets occurs. Since the company’s asset-backed credit facility, term loan and 2027 notes all mature within seven months of one another, management will likely try to find a comprehensive out-of-court solution for its capital structure.

Jeld-Wen has retained Evercore as financial advisor and Kirkland & Ellis as legal counsel. A group of term loan lenders has hired Moelis and Gibson Dunn & Crutcher, and a group of unsecured bondholders has mandated Houlihan Lokey and Davis Polk & Wardwell.

The company said it aims to address its near-term maturities before they start to go current in December.

Investment Thesis

JELD 4.875% unsecured notes due 2027 currently trade at ~80.25 yielding approximately 20% as of May 13. Candid Value believes the 2027 unsecured notes are uniquely positioned to benefit from their temporal seniority by gaining liens on assets in exchange for a maturity extension. Candid Value contends that the purchase of the 2027 notes should result in capital gains capture along with an interest rate increase. In potential current and future bankruptcy scenarios, the 2027 notes are likely the fulcrum security, resulting in post-reorganization equity, which offers significant upside to Jeld-Wen’s mid-cycle earnings potential. However, the 2027 notes’ fulcrum security claim in such bankruptcy scenarios could be diluted by a large DIP facility financing, an elaborate rights offering, fees and other mechanisms used to seize value in bankruptcy proceedings.

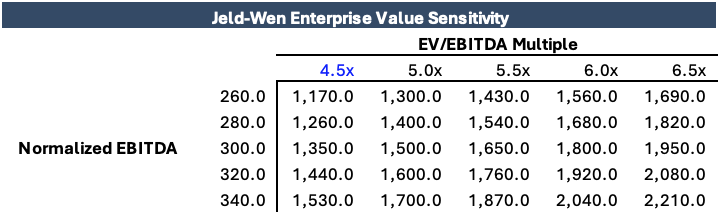

While current debt prices imply an enterprise value for the business of approximately $925 million as of May 13, Candid Value believes the company’s EV during a more normalized mid-cycle earnings period could range from $1.5 billion to $1.8 billion based on an adjusted EBITDA of $300 million and EV/EBITDA multiples of 5x to 6x. We expect mid-cycle adjusted EBITDA margin to recover to a more normalized level of approximately 8%, when accounting for the forced divestiture of its 20%+ margin Towanda business (the first ever antitrust lawsuit brought on by a competitor, rather than a US governing body, which resulted in a court-ordered divestiture). Our base case does not factor in any improvement from current cost and efficiency initiatives, providing further valuation upside if realized. Enterprise value sensitivities are shown below.

Although Jeld-Wen has previously attempted to mend its highly fragmented and inefficient manufacturing network (a byproduct of its aggressive roll-up strategy), CEO Bill Christensen recently admitted that this initiative has “suffered from historical underinvestment.” Yet, management may finally be making headway with its on-time, in-full, or OTIF, rate, which is a supply chain metric for orders delivered accurately and on schedule, exceeding 90% in March for its North American operations. Management’s goal is to reach an OTIF rate of greater than 95%.

A high OTIF rate may not guarantee cost savings on its own, but it builds the operational foundation required to achieve the company's goals of improving efficiency and cutting costs. However, given management’s track record of underperformance on this front, even if it falls short on its cost initiatives, a rebound to historical mid-cycle margins would be enough to support our enterprise value range above. Candid Value estimates that Jeld-Wen’s current capital structure would remain covered at an EBITDA floor of $270 million based on a depressed EV/EBITDA multiple of 4.5x.

Capital Structure Scenarios

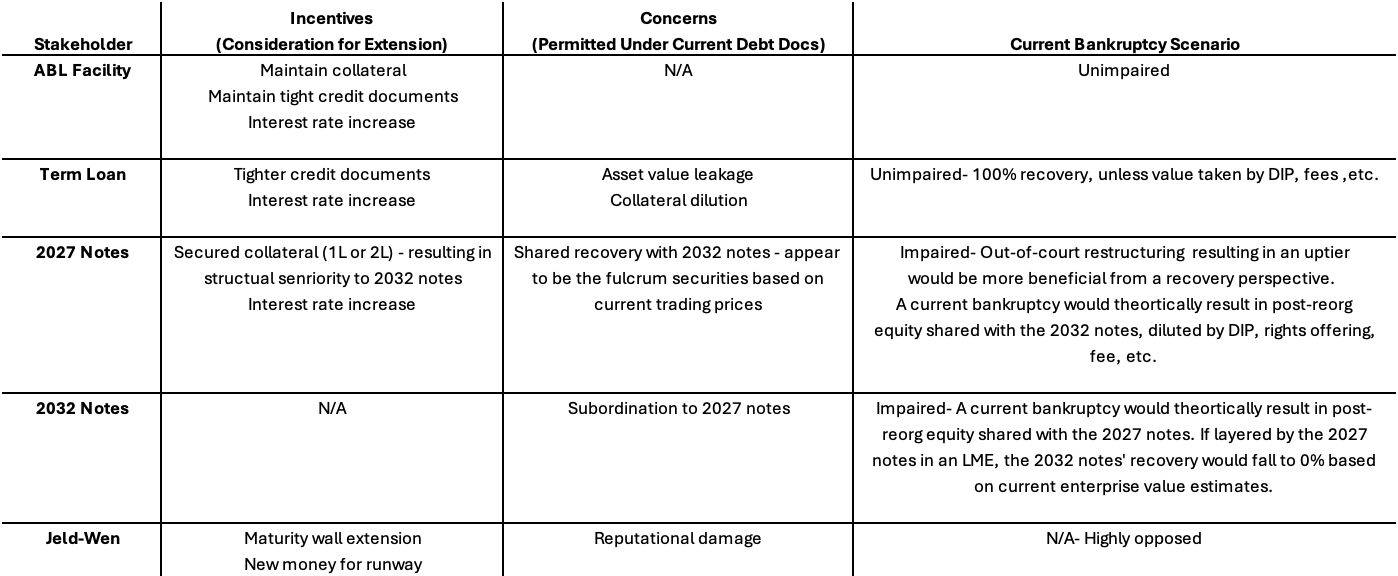

Jeld-Wen requires a holistic capital structure solution, which would include extending the maturities of its ABL facility, term loan and 2027 notes, and a new money injection to lengthen runway.

Candid Value believes:

ABL lenders are generally indifferent about extending their maturity as long as they maintain their collateral, albeit at a lower commitment base, along with price and fee increases.

Term loan lenders want to prevent asset value leakage or dilution, which is currently permitted under their credit agreement. Candid Value suspects term lenders will be satisfied with a tighter credit agreement.

2027 noteholders want to protect their downside risk by gaining collateral security. They would also want preferential treatment above the 2032 notes. Currently, both notes rank pari passu at the unsecured level, so any collateral support that the 2027 notes receive will move them ahead of the 2032 notes, resulting in them being the sole fulcrum security from currently being joint fulcrum securities with the 2032 notes.

2032 noteholders don’t hold any current negotiating leverage.

Management wants to extend the maturity wall and runway in an out-of-court setting.

Candid Value outlines the incentives and concerns for each Jeld-Wen stakeholder during capital structure negotiations in the diagram below, along with potential outcomes in a current bankruptcy scenario. We view the likelihood of Jeld-Wen filing for bankruptcy as minimal, nevertheless, assessing bankruptcy outcomes is essential from a game theory perspective.

Candid Value believes that the potential overhang of an aggressive LME, given Jeld-Wen’s lenient credit documents, will serve as a strong incentive for holders of the term loan and 2027 notes to get a consensual maturity wall extension completed on negotiated terms.

As a result, Candid Value contemplates a relatively “simple” comprehensive capital structure solution for Jeld-Wen that provides each stakeholder with enough incentive to extend their maturities, rather than the company using aggressive LME tactics to effectuate a deal. This “simple” transaction includes the uptiering of 2027 unsecured notes into second lien debt due 2031 at par, although it may be possible for the company to capture a haircut; the amendment and extension of the term loan to 2031 with a significantly tighter credit agreement protecting against aforementioned LME risks; and the amendment and extension of the ABL facility to 2031 with $100 million raised under a new-money first-in, last-out, or FILO, facility.

Alternatively, the company could raise new money at the reinforced first lien term loan level under the new strict credit documents if the lenders believe such new debt would trade at par. Candid Value suspects that the company will look to have all of its newly issued or amended debt mature at or around 2031, with the potential to stagger the maturities of each security if need be. We also expect that the new debt will bear interest at significantly higher rates than its current debt, most likely with PIK components given the company’s projected FCF burn.

The company might deploy certain coercive tactics to combat holdout risk of the term loan lenders and 2027 noteholders. However, these maneuvers would likely result in a similar recovery waterfall as the “simple” transaction, but with more bells and whistles.

In the following scenarios, Candid Value assumes 100% consent of its ABL lenders, making the term loan credit agreement the most restrictive debt document in the structure. Jeld-Wen said it would pay down “much” of the ABL’s balance by year end, which had $40 million outstanding as of March 28. The company has not historically utilized its ABL facility for the repayment of debt.

Jeld-Wen initiated the comprehensive review of strategic alternatives for its European business in November 2024, which could include the sale of the segment. The company has not announced any updates from the review, but Candid Value believes it is unlikely that the company will realize the full potential of this business by monetizing it at or around current bottom-of-the-cycle earnings and multiples. The European business could potentially be an asset utilized in drop-down or pari-plus transactions.

Regarding an alternative liquidity lever, the company has uncapped sale-leaseback capacity under its current debt documents, so long as the assets are not constituted as ABL priority collateral.

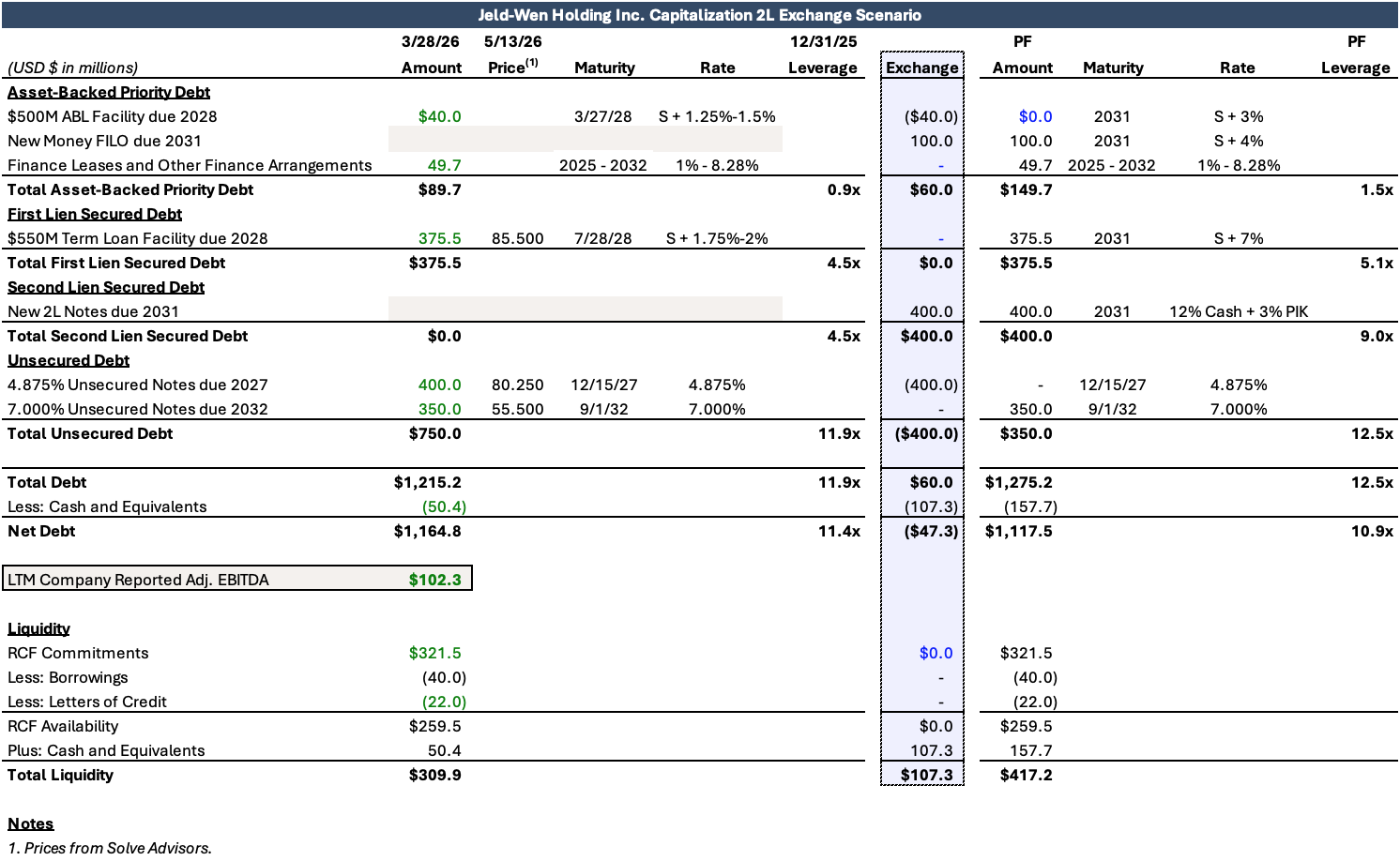

2L Uptier Scenario

Our “simple” transaction would include the following:

An uptier exchange for the 4.875% unsecured notes due 2027 into second lien debt at par with a 2031 maturity and an interest rate increase;

An amend-and-extend for the term loan due 2028 with a reinforced credit agreement protecting against collateral dilution and asset value leakage, among other items, along with an interest rate increase in exchange for a maturity extension to 2031;

The extension of its ABL credit facility to 2031 in exchange for interest rate and fee increases, potentially with a lower commitment base; and

A new-money raise through an ABL FILO facility of $100 million.

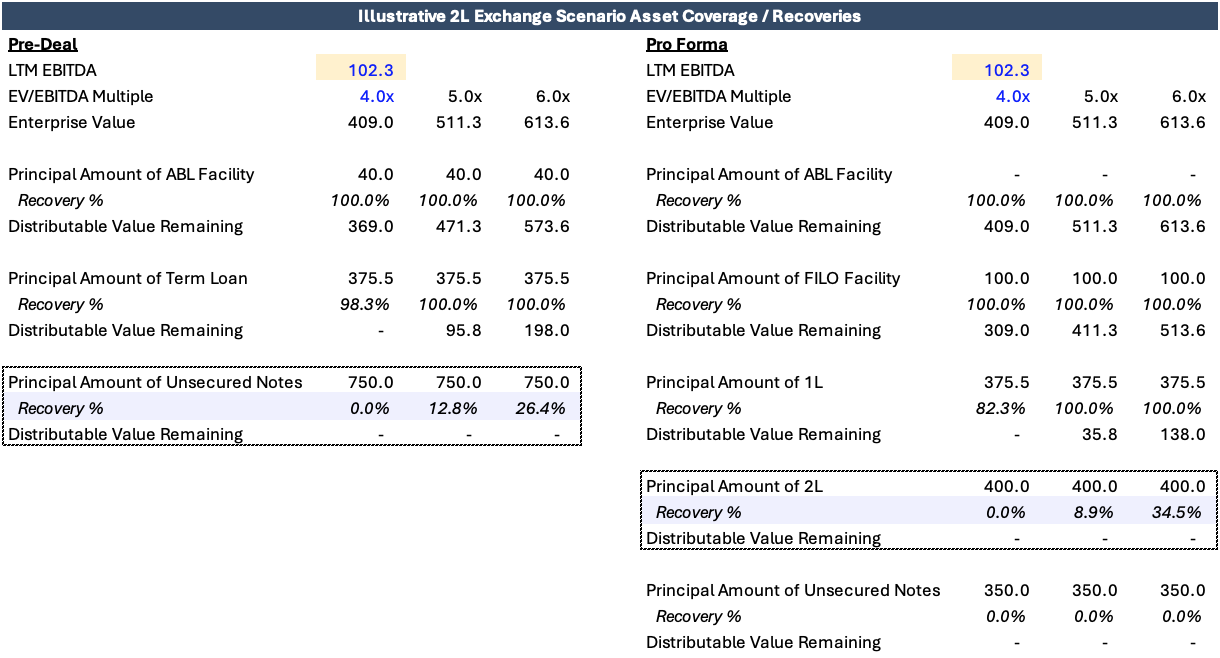

We assume that Jeld-Wen will use its expected FCF for the remainder of the year of $47.3 million to pay down its $40 million ABL borrowings. The second-lien uptier scenario, assuming the full participation of 2027 noteholders, is illustrated below:

In this scenario, the previously unsecured 2027 notes will receive liens on Jeld-Wen’s assets on a second-lien priority basis. While the new money component will reduce the 2027 notes’ recoveries under current valuations, the notes will rank senior to the 2032 notes going forward, no longer ranking pari passu. This would push the 2027 notes up the priority waterfall as shown below.

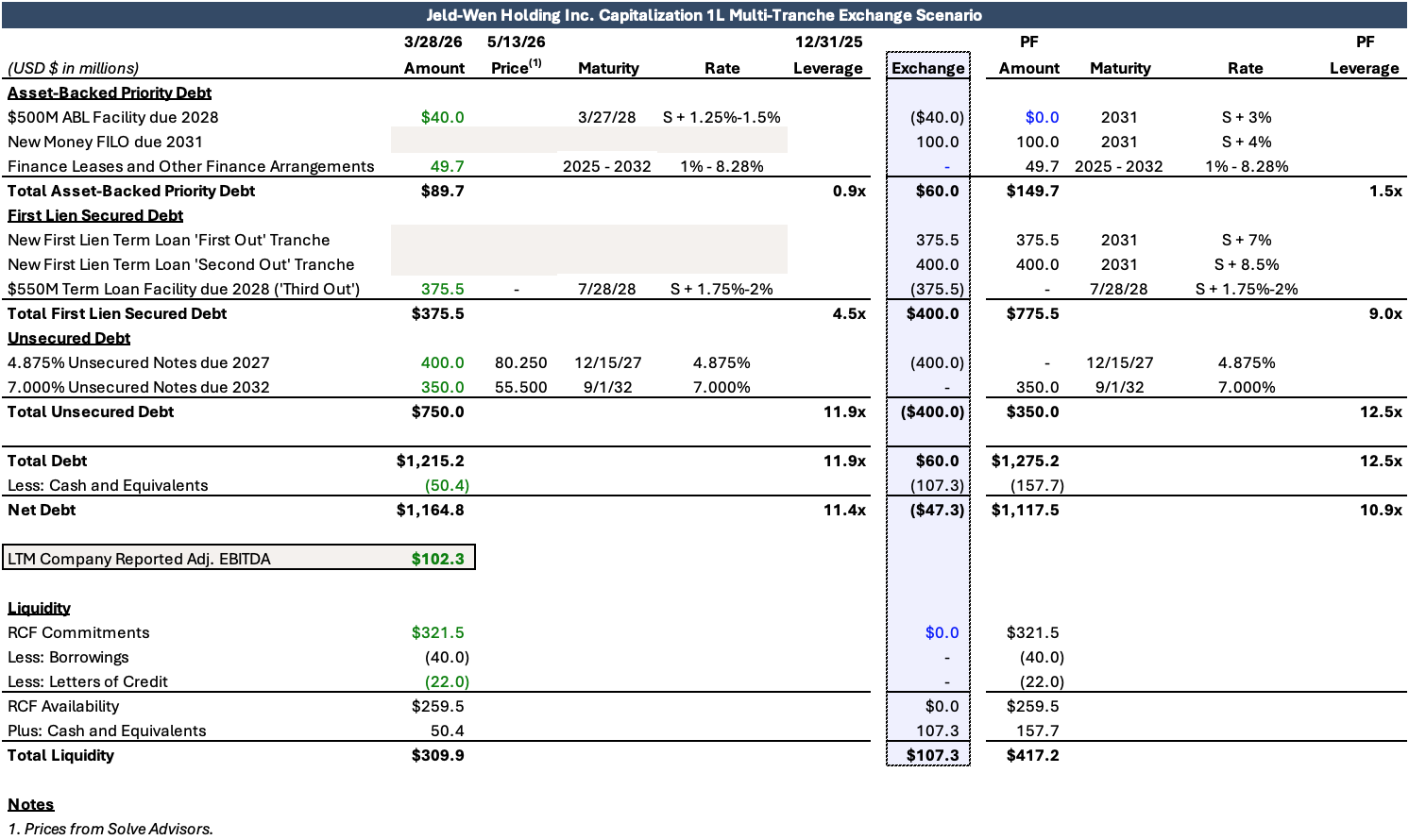

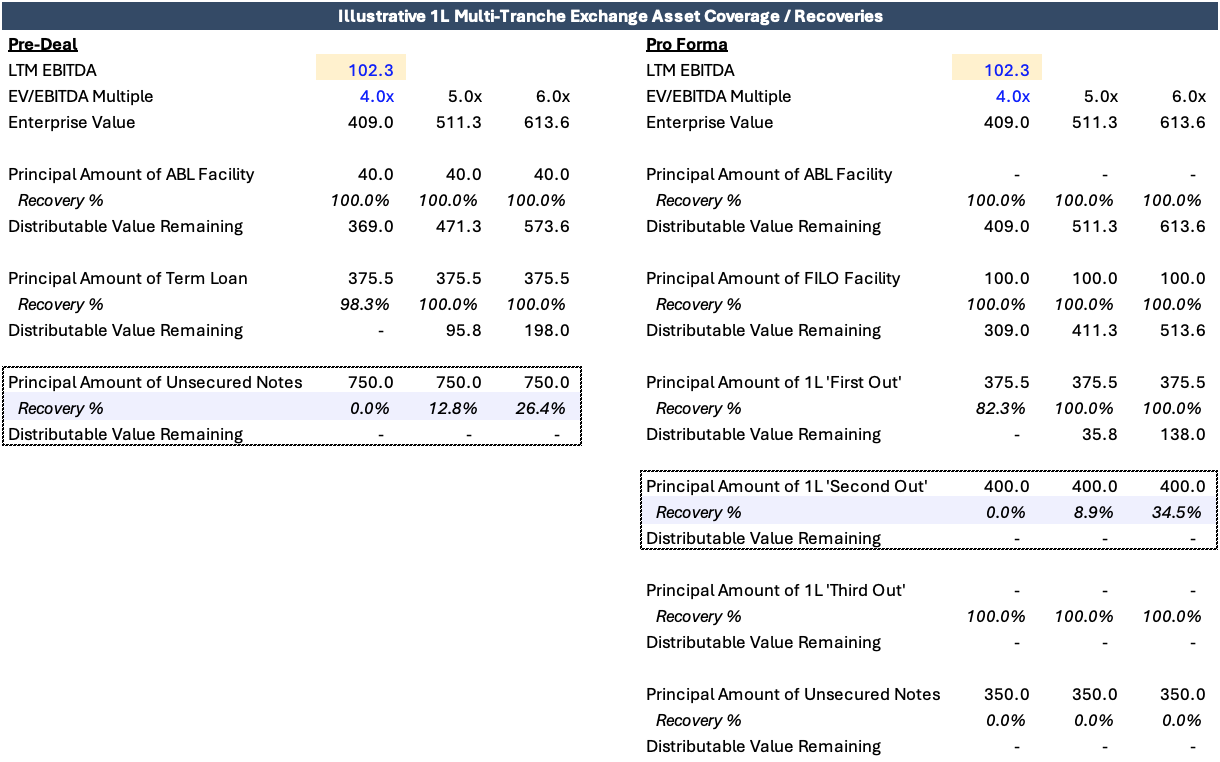

1L Muli-Tranche Uptier Scenario

Given the conflicting stakeholders’ incentives, sizable holdouts could cause the transaction mentioned above to fall through.

The company could mitigate the term lenders’ holdout risk by mentioning an arsenal of LME strategies that could diverge asset value or dilute their existing collateral through a drop-down, the utilization of a double-dip/pari-plus structure or an uptier transaction, significantly impairing nonparticipating term lenders’ asset coverage.

The company could alleviate the risk of holdout by 2027 noteholders by offering the 2032 notes the opportunity to uptier as well, allowing the 2032 notes to exchange into the same priority paper as the 2027 notes. This would likely involve a two-phase transaction with the company’s intention to uptier the 2032 notes voiced at the onset of the offering. Phase 1 would offer the uptiering to the 2027 notes and the second phase would open the exchange to the 2032 notes, while still prioritizing the 2027 notes; the total amount of new notes would be capped at $400 million, which is the amount of 2027 notes outstanding at quarter end.

Bringing these concepts together, Candid Value contemplates an alternative transaction that could address holdout risk through a multi-tranche first-out, second-out and third-out structure within the existing term loan as follows:

An exchange for term loan lenders into a first-out term loan tranche maturing in 2031 at an increased interest rate;

An uptier exchange for 2027 notes into a second-out term loan tranche maturing in 2031, through a two-phase process discussed above, allowing 2032 notes to uptier in the second-phase capped at $400 million of second-out loans issued; and

Nonparticipating term loan lenders left as a third-out term loan tranche and nonparticipating 2027 notes and 2032 notes left outstanding.

This first-lien multi-tranche uptier scenario, assuming the full participation of 2027 noteholders, is illustrated below:

In this scenario, the previously unsecured 2027 notes will receive liens on Jeld-Wen’s assets on a second-out first-lien priority basis. Similar to the previous transaction, the new money component will reduce the 2027 notes’ recoveries under current valuations, but the notes will be better off than before from a waterfall standpoint as shown below.

Jeld-Wen has the flexibility to add more phases and tranches to the transaction, applying certain discount exchange rates at different levels, or a new-money component at the first-out level. The term loan credit agreement allows for the possibility of non-pro-rata deals as well.

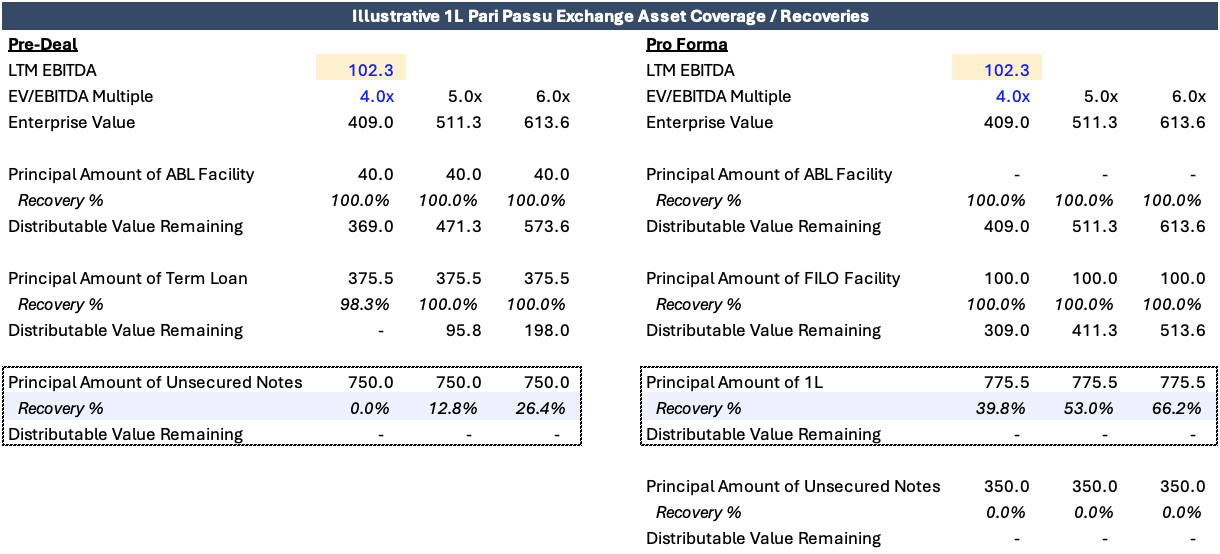

1L Pari Passu Uptier Scenario

While Candid Value believes the following scenario is unlikely, Jeld-Wen’s credit documents allow for the uptiering of the 2027 notes into first lien debt pari passu with existing term loans. However, this would leave term loan lenders very unpleased and would have to be followed up by an aggressive LME to deal with the loans or a miraculous rebound in Jeld-Wen’s business ahead of the loan’s maturity in July 2028. This first-lien pari passu uptier scenario, assuming the full participation of 2027 noteholders, is illustrated below:

In this scenario, the previously unsecured 2027 notes will receive liens on Jeld-Wen’s assets on a first-lien priority basis, ranking pari passu with the existing term loans. This scenario would significantly increase the 2027 notes’ recoveries while substantially diluting the term loans’ recoveries. The priority waterfall before and after the transaction at current EV valuations is shown below.

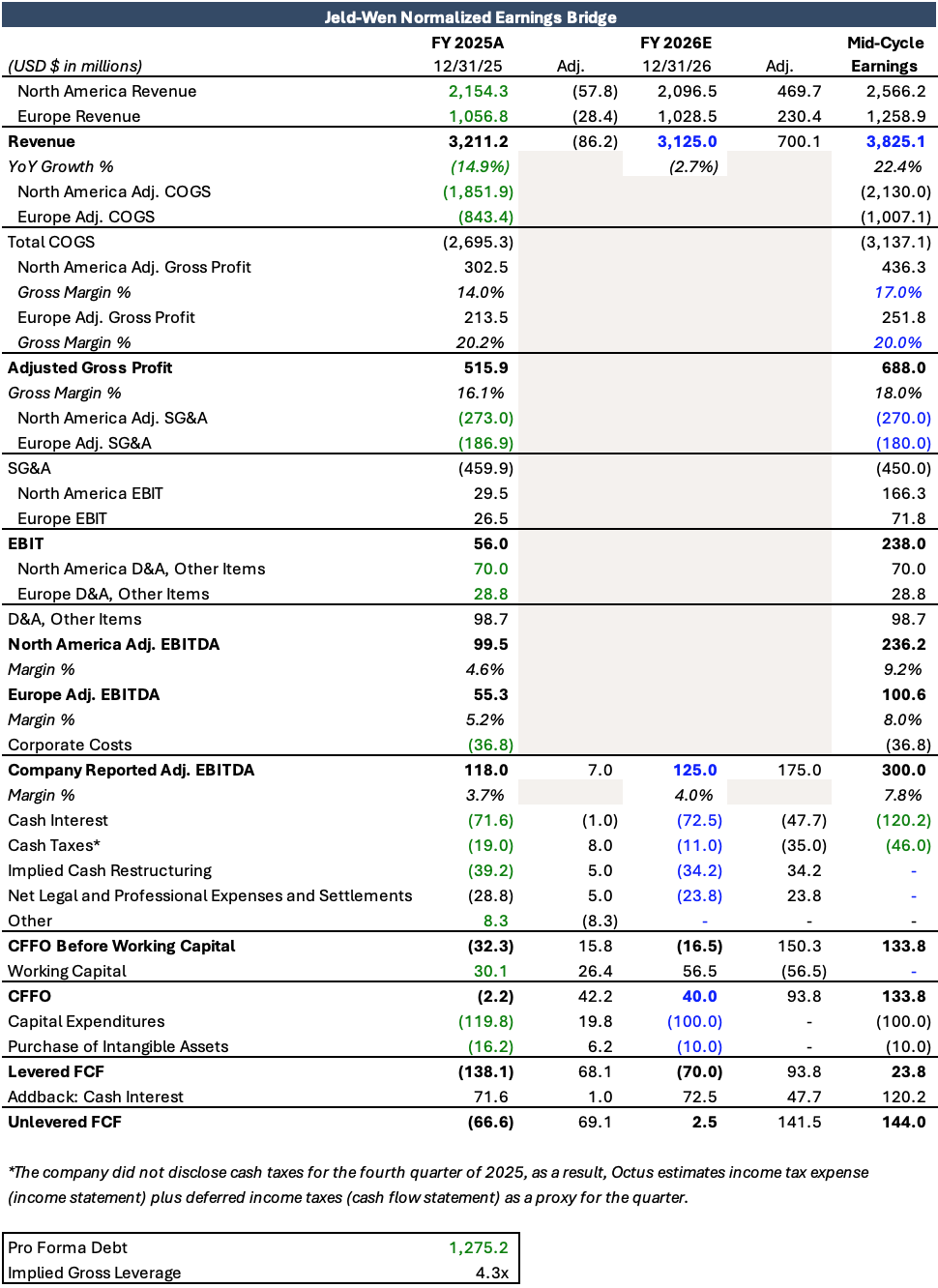

Jeld-Wen Mid-Cycle Enterprise Value Estimated at $1.5B-$1.8B

Based on historical financials, Candid Value estimates that Jeld-Wen can generate revenue of approximately $3.825 billion and adjusted EBITDA of $300 million during a normalized earnings period, implying a pro forma debt to EBITDA multiple of 4.3x. This equates to unlevered FCF of approximately $144 million, which would support elevated interest payments of approximately $120 million. Upon a mid-cycle recovery, the company would likely refinance its capital structure. A mid-cycle earnings bridge is shown below.

Candid Value assumes North American adjusted gross margin of 17% and European adjusted gross margin of 20%, compared with average adjusted gross margin from 2022 to 2025 for North America of 17.1% and Europe of 19.4%. Candid Value keeps North American gross margin below the company’s historical average, but maintains European gross margin at the current level for the TTM period ended March 28 of 20.2%. We assume European margins will not slip further from current levels. We straightline selling, general and administrative costs totaling approximately $450 million and corporate costs of approximately $37 million.

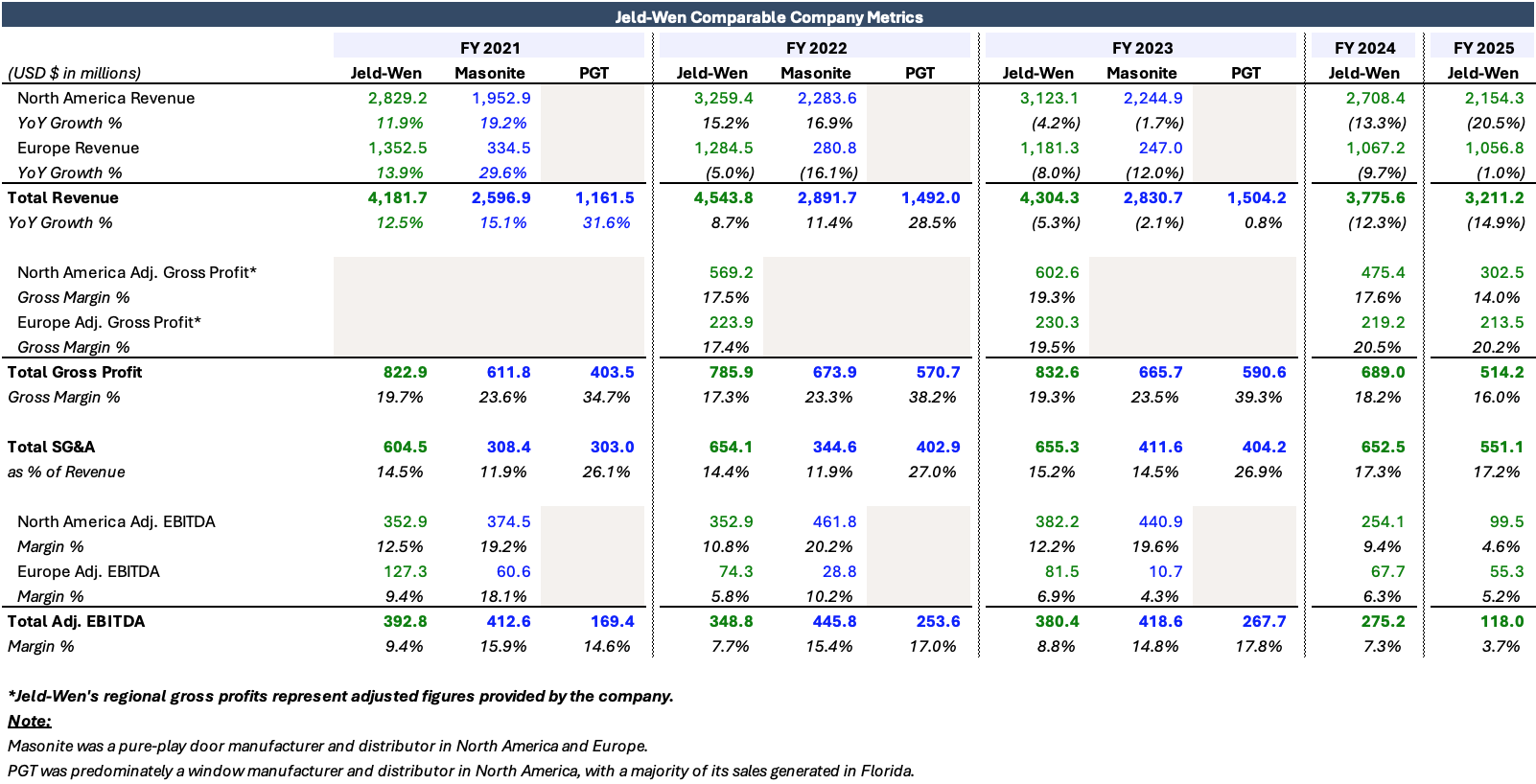

Candid Value estimates an enterprise value for Jeld-Wen of $1.5 billion to $1.8 billion based on an adjusted EBITDA of $300 million and EV/EBITDA multiples of 5x to 6x. We believe our EV/EBITDA multiple range is on the lower end for a windows and doors manufacturer. Jeld-Wen’s competitors have been acquired at EV/EBITDA multiples ranging from 8x to 12x.

PGT Innovations was acquired at an 11.5x EV to adjusted EBITDA for the TTM period ended Sept. 30, 2023 multiple after a bidding war between Miter Brands and Masonite. According to the proxy statement, Evercore estimated an EV to TTM adjusted EBITDA multiple range for precedent transactions of 8.5x to 11.5x. Based on public comparable companies, Evercore calculated an EV to 2024E adjusted EBITDA multiple range of 7x to 9x.

Coincidentally, Masonite was later acquired at an 8.6x EV to adjusted EBITDA for the full-year 2023 (pro forma the expected contribution from Fleetwood Aluminum Products LLC of $35 million) multiple. According to the proxy statement, Goldman Sachs estimated a range of EV to TTM adjusted EBITDA multiples for precedent transactions of 8x to 10.3x. Goldman Sachs calculated a range of EV to next-12-month EBITDA of 6.25x to 7.25x based on public company comparables.

Jefferies estimated an EV to TTM adjusted EBITDA multiple range for precedent transactions of 6.6x to 11x and selected a range of 8x to 10x for Masonite’s 2023 EBITDA based on their judgement. Jefferies calculated an EV to 2024E adjusted EBITDA multiple range for public comparable companies of 6.5x to 12.3x, ultimately selecting a range of 6.5x to 7.5x for Masonite’s 2024E EBITDA based on their judgment.

Albeit, Jeld-Wen’s year-over-year top-line growth and margins have underperformed relative to Masonite and PGT in the years leading up to their acquisitions in 2024. We suspect Jeld-Wen warrants an EV/EBITDA multiple closer to 6x during a normalized earnings period. Summary financials metrics for Jeld-Wen, Masonite and PGT are shown below: