B. Riley: Long 6% RILYT Notes Due 2028 / 5.25% RILYZ Notes Due 2028

Long 6% RILYT Notes Due 2028 at ~18.02 / 5.25% RILYZ Notes Due 2028 at ~16.55 as of April 10, 2026

〰️

Long 6% RILYT Notes Due 2028 at ~18.02 / 5.25% RILYZ Notes Due 2028 at ~16.55 as of April 10, 2026 〰️

Situation Overview

BRC Group Holdings Inc. (NASDAQ: RILY), f/k/a B. Riley Financial Inc., is a small-cap and middle-market investment bank and institutional brokerage at its core, with niche operations in the telecommunications and retail spaces, and an investment portfolio rooted in a merchant banking partnership model. The company has faced heavy regulatory scrutiny and relatively underperformed its peers over the last several years. In a bid to course-correct, BRC focused its efforts on divesting noncore assets and “realign[ing its] operating businesses towards financial services and capital markets.”

Consequently, the company carved out B. Riley Securities Holdings Inc., or BRS, which houses its investment banking and brokerage businesses, in March 2025, retaining 89.4% ownership on a fully diluted basis. Candid Value suspects that management’s objective was to isolate BRC’s core operating business from its investment portfolio, in hopes of the market valuing the entity closer to industry enterprise value to EBITDA multiples of 9x to 13x. However, we contend that BRS should trade at a discount to its larger public “elite” boutique peers given its riskier mandates, smaller client size and recent underperformance.

The investment banking sector was characterized as a “deal desert” in 2022 and 2023, followed by a gradual reopening in 2024 and a stronger rebound in 2025. While BRC felt the wrath of the “deal desert,” it was unable to partake in the subsequent rebound as capital markets’ services and fees revenue was down 17.3%, 22.7% and 15% year over year in 2025, 2024 and 2023, respectively. In comparison, relevant segment revenues at Evercore, Moelis, Piper Sandler and PJT were up 30%, 27%, 24.5% and 14.8% year over year, respectively, in 2025. Candid Value believes that the aftermath of the Franchise Group, or FRG, bankruptcy and fallout of securities fraud conspirator Brian Kahn, coupled with persistent Security and Exchange Commission filing delays, continue to hinder the company’s deal flow. We believe an appropriate EV/EBITDA multiple range for BRS is 4.5x to 6.5x.

BRC started to garner substantial short interest in February 2023, when Wolfpack Research published a short report highlighting numerous risky loans held by the company. The situation finally imploded during the FRG and Kahn saga. In January 2024, Kahn resigned as CEO and a member of the board of Freedom VCM (parent holding company of FRG) amid the securities fraud turmoil at Prophecy Asset Management. In November 2024, Freedom VCM filed for Chapter 11, practically wiping out BRC’s investments in FRG worth $481.6 million. A year later in November 2025, the U.S. Attorney’s Office for the District of New Jersey charged Kahn with securities fraud, which he pleaded guilty to a month later.

These events triggered a flurry of lawsuits, along with investigations by the SEC and Financial Industry Regulatory Authority. Recently, the Delaware Court of Chancery dismissed the shareholder derivative complaint regarding the company’s conduct advising FRG on March 30, alleviating significant legal risk. Nevertheless, active SEC and FINRA investigations, alongside a federal securities fraud class action and several retail investor class action lawsuits, remain ongoing against BRC, Bryant Riley and management. Despite this legal overhang, the current market consensus suggests a low probability that BRC will be convicted of wrongdoings. The prevailing view is that if a conviction were imminent, it would have already occurred during the Kahn and Prophecy Asset Management proceedings.

Aside from pending legal and regulatory risks, the company has filed every 10-Q late since the second quarter of 2024 and every 10-K late since 2022. These consistent delays, especially during a comprehensive operational restructuring (divestitures listed below), have severely clouded visibility into BRC’s residual asset value. Additionally, the structure is primarily funded by “baby bonds,” generally intended for and broadly held by retail investors, which has deterred many larger institutional investors away from the credit. Candid Value believes that this perfect storm of information lag, valuation complexity and lack of institutional attention, has resulted in a unique buying opportunity for BRC’s materially mispriced unsecured bonds.

Net Debt Has Decreased $480M Since Year-End 2024 Through Asset Sales, Investment Proceeds & Uptier, Debt-to-Equity Exchanges

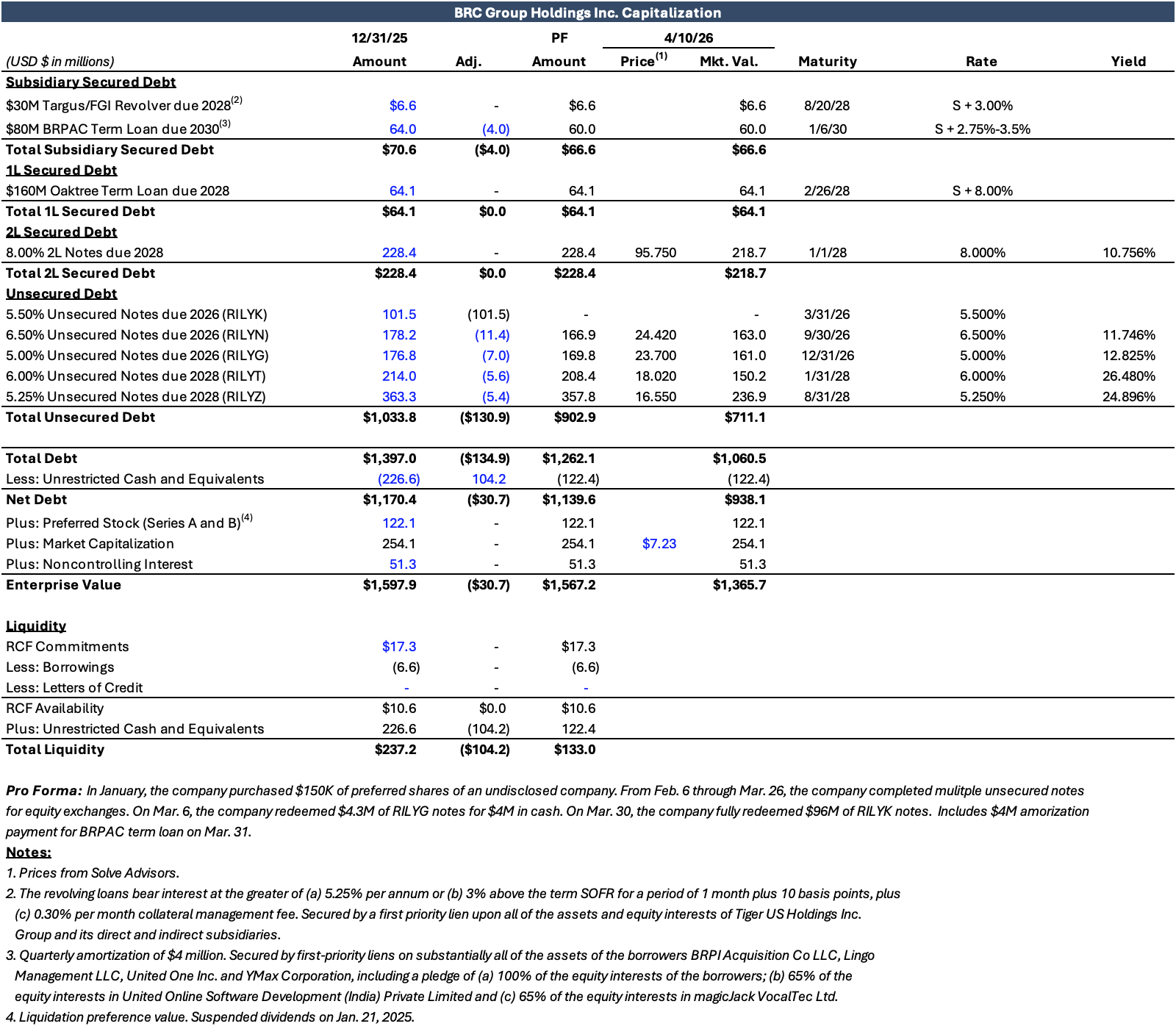

Candid Value estimates that as of March 31, BRC has approximately $1.262 billion of total debt, comprising $66.6 million of secured subsidiary debt, $292.5 million of secured corporate debt and $902.9 million of unsecured corporate debt, and unrestricted cash of $122.4 million before potential first-quarter 2026 cash generation. The company has preferred stock outstanding at a liquidation preference amount of $122.1 million as of Dec. 31, 2025, and a market capitalization of approximately $254.1 million as of April 10.

In 2025, divestitures, investment and loans receivable proceeds totaled $212.4 million, $27.6 million and $57.4 million, respectively, which were predominantly used to repay debt.

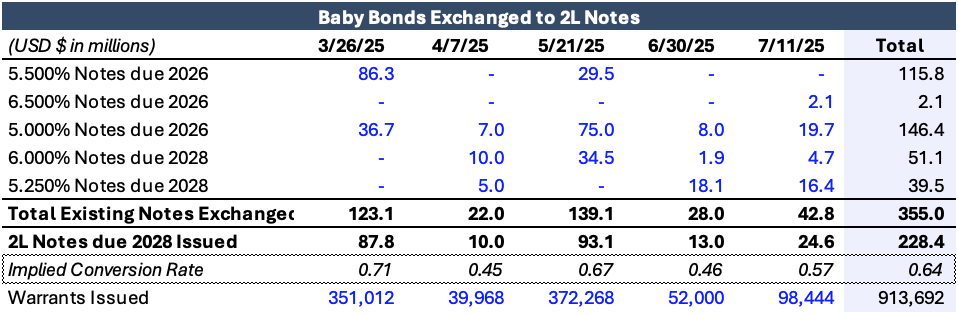

From March 26, 2025, through July 11, 2025, the company uptiered an aggregate principal amount of $355 million of baby bonds into $228.4 million of 8% second lien notes due 2028 at an average exchange rate of 64% and 913,692 warrants through five private-exchange transactions. The uptiering exchanges are shown below. According to the Oaktree term loan’s credit agreement, BRC has capacity to issue $21.6 million of additional 2L notes for a total not to exceed $250 million.

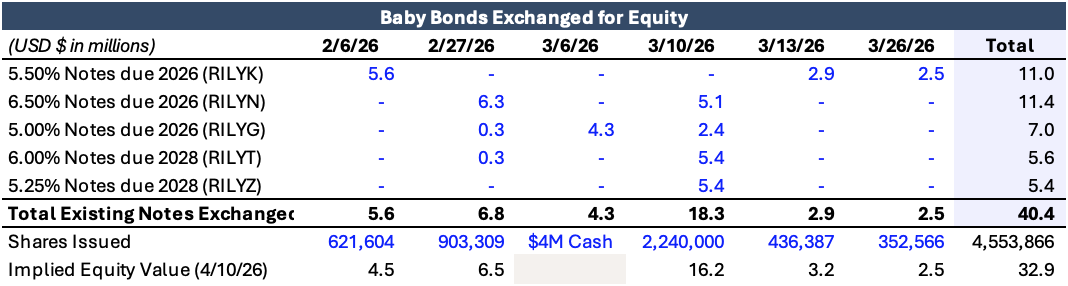

From Feb. 6 through March 26, the company exchanged an aggregate principal amount of $36.1 million of baby bonds into approximately 4.6 million common shares, which have a total market value of $32.9 million as of April 10. On March 6, the company repaid $4.3 million of 5% RILYG notes due 2026 with $4 million in cash. The debt-to-equity exchanges are shown below.

BRC’s capital structure pro forma a $150,000 preferred share purchase of an undisclosed company in January; the debt-for-equity exchanges; the RILYG partial paydown; the full redemption of $96 million of 5.5% RILYK unsecured notes due 2026 on March 30; and a $4 million amortization payment on the BRPAC term loan on March 31 is shown below.

Investment Thesis

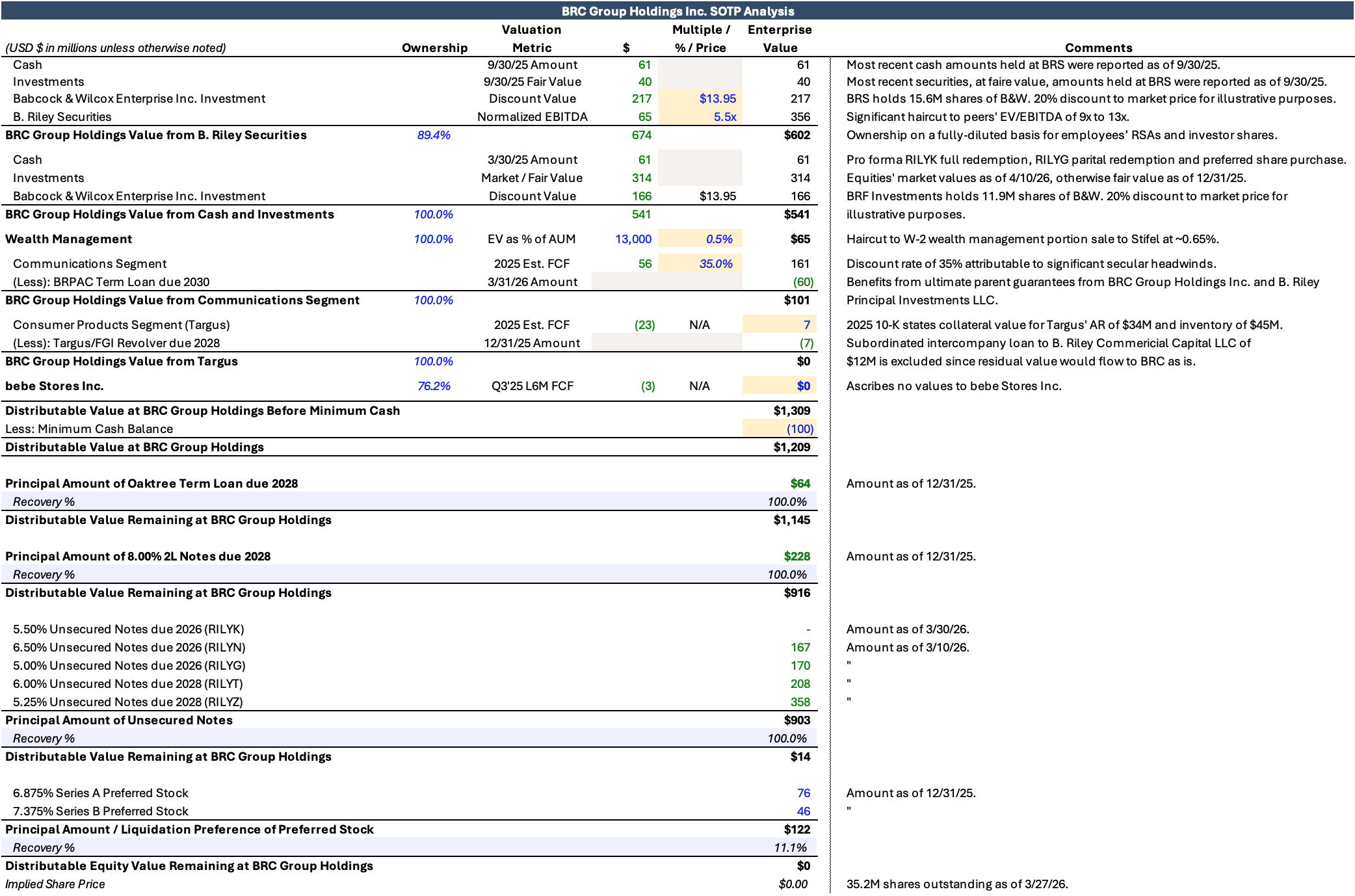

RILYT 6% unsecured notes due 2028 currently trade at ~72.1 yielding 26.5% and RILZ 5.25% unsecured notes due 2028 currently trade at ~66.2 yielding 24.9% as of April 10. Based on a sum-of-the-parts analysis, Candid Value estimates that total distributable value at BRC Group Holdings Inc. is approximately $1.2 billion as of April 10, enough to cover its total corporate funded debt of approximately $1.2 billion as of March 31, implying 100% coverage for its unsecured notes. We believe the company will be able to either refinance or repay its unsecured bonds at maturity.

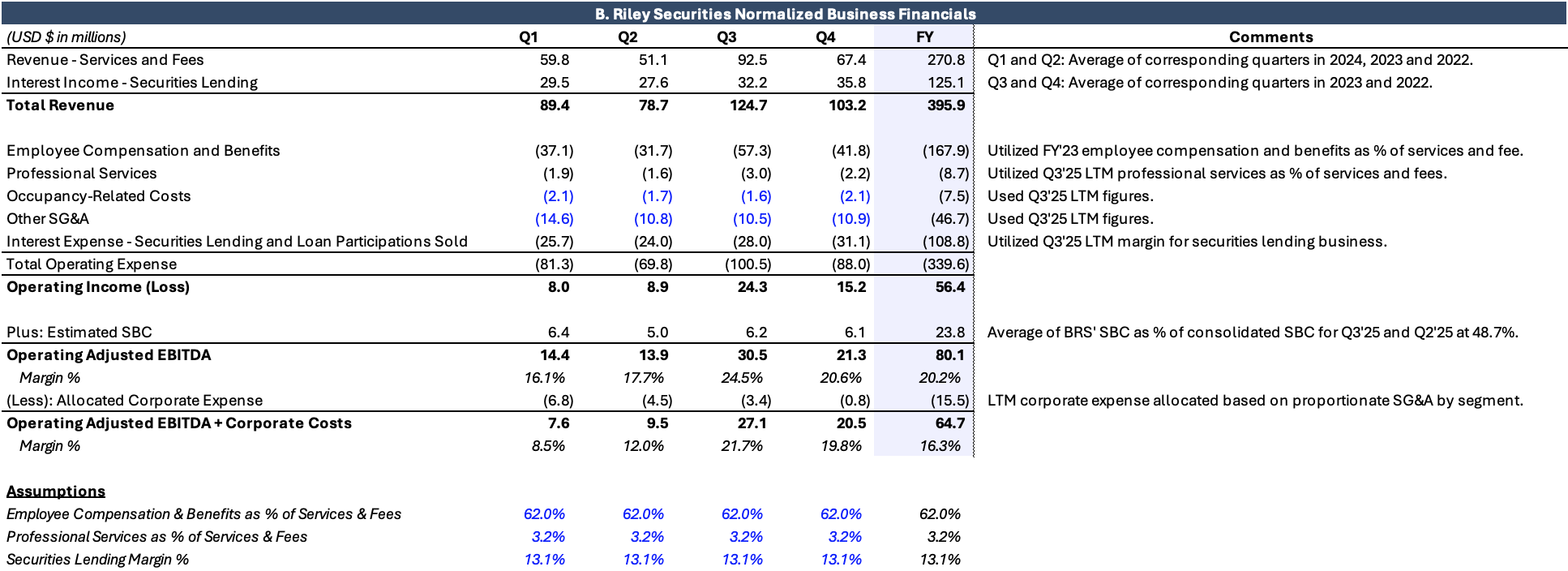

A majority of the value at BRC is attributable to its investment portfolio valued at $832.5 million as of April 10, of which Babcock & Wilcox’s equity accounts for $478.7 million, and its core investment banking and brokerage business valued at $355.6 million based a normalized EBITDA (including an allocated portion of corporate expenses) of $64.7 million and an EV/EBITDA multiple of 5.5x. Candid Value’s SOTP analysis for BRC is shown below.

BRC’s valuation is highly levered to its Babcock & Wilcox equity investment, which currently trades at a seven-year high of $17.44 per share as of April 10. Candid Value estimates that the company’s unsecured notes retain 100% recoveries at a B&W price floor of $13.43 per share, a 23% cushion to its current share price. Every $1 decrease in B&W’s common share price from then on would result in a 286-bps decrement to the unsecured notes recovery, according to Candid Value’s estimates. The unsecured notes’ recoveries sensitized at declining B&W share prices are shown below.

We believe our BRC valuation is conservative. We utilize relatively low valuation multiples for every operating segment compared with their respective peers and handicap certain investments, notably B&W equity at $13.95 per share (a 20% discount to the current price) and Great American Group investment at a hypothetical liquidation at book value, or HLBV, amount of $83.3 million as of Dec. 31, 2025. Even at these “bear-case” adjacent valuations, the baby bonds remain covered.

The dismissal of the shareholder derivative lawsuit, coupled with timely SEC filings going forward, could mend previous reputational harm, serving as a tailwind to deal flow, affording BRS a higher multiple closer its industry peers moving forward. The company also highlighted holdings of SpaceX within its wealth management segment, which the company will generate a carried interest on. Its SpaceX carried interest could produce substantial fees for the wealth management business, while also restoring goodwill and potentially leading to assets under management, or AUM, growth.

During the fourth quarter of 2025 earnings call, management explained that the HBLV amount for GA Group severely undercuts the true value of the business. Last week, GA Group acquired G2 Capital Advisors, nearly doubling the size of the company. Since both companies are private and no details were disclosed about the transaction, it’s difficult to decipher potential investment appreciation. Nevertheless, we believe GA Group’s current valuation within our SOTP analysis is undervalued.

While we believe there is ample current value at BRC to cover its unsecured debt, these variables serve as catalysts to boost distributable asset value further.

Sum-of-the-Parts Analysis

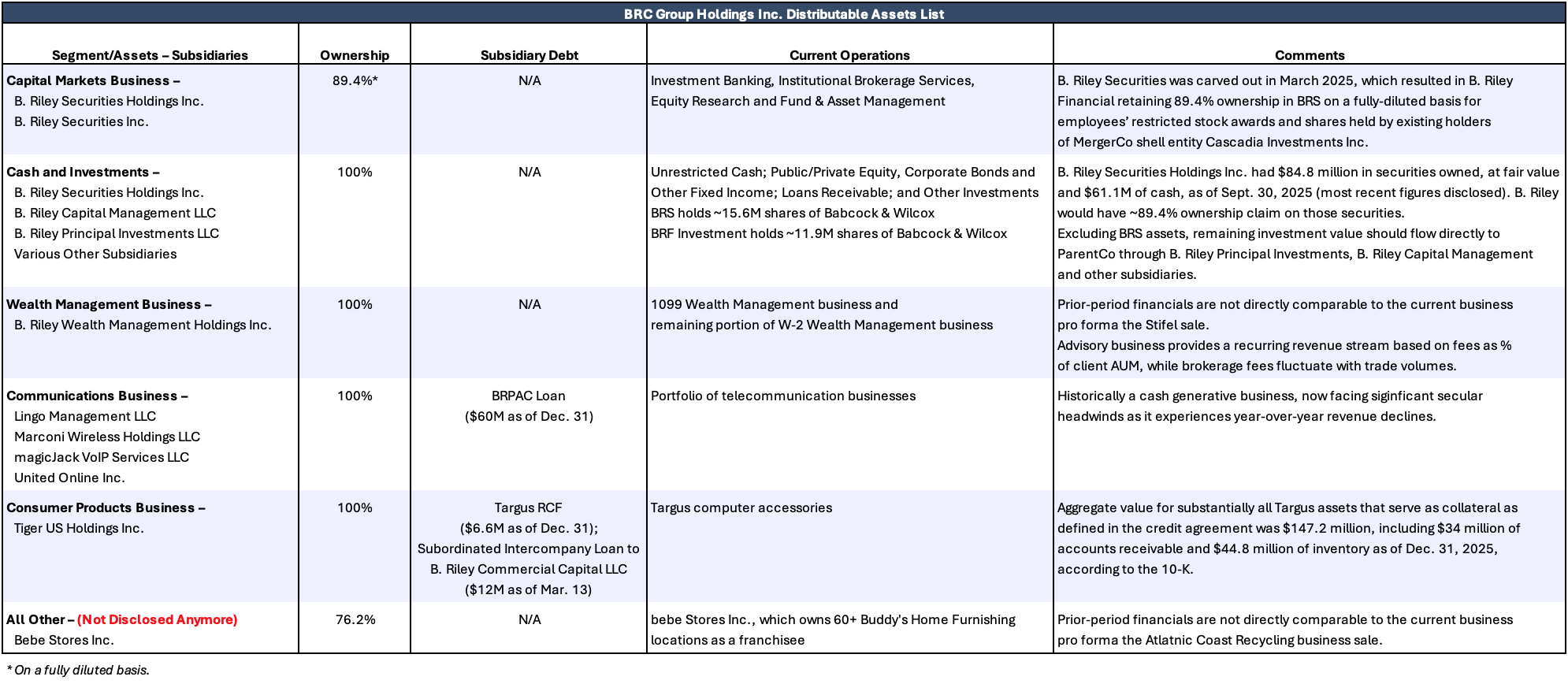

A series of divestitures at BRC has made it difficult to ascertain remaining asset value. These sales have made certain year-over-year comparisons of its segment results complicated since the company has not restated its financials to reflect such changes.

Recent divestitures include the GlassRatner and Farber advisory businesses for $117.8 million in June 2025; the W-2 wealth management business for $26 million in April 2025; Atlantic Coast Recycling for $68.6 million in March 2025; a securitization financing transaction of Six Brands and Hurley, Justice, and Scotch & Soda for $189.3 million in October 2024; and the sale of a 52.6% ownership stake in the liquidator Great American Group for $203 million also in October 2024.

We have compiled the following description of BRC’s current businesses:

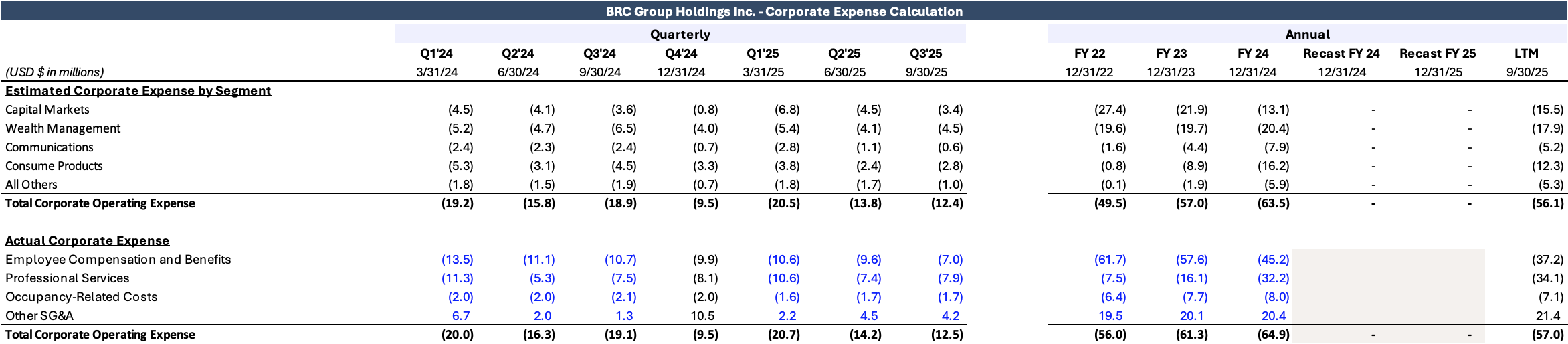

BRC consistently spends approximately $60 million on corporate expenses annually. Candid Value contends that any accurate valuation of BRC must account for these costs, given their recurring nature and relative size. In this exercise, we allocate corporate expense to each segment, on the basis of its corresponding operating expense line item and the pro rata breakdown of that expense across segments. The company stopped providing corporate expenses in the fourth quarter of 2025, so Candid Value utilized last-twelve-month ended Sept. 30, 2025, estimates as a proxy for go-forward corporate expenses by segment.

While this method might deflate segment valuations, we believe it captures the impact of corporate expenses more effectively than deducting a lump sum at the end of the SOTP analysis. The company has not disclosed much information as to what these corporate costs entail. We believe our inclusion of these expenses in this way provides a margin of safety to our analysis in case these corporate expenses are more closely tied to segment operations than alluded to. Corporate expense allocations by segment are shown below.

B. Riley Securities’ EV Estimated at $275M to $450M, Excluding Cash and Investments

For valuation purposes, we maintain that BRC owns 89.4% of B. Riley Securities Holdings Inc., or BRS, on a fully diluted basis assuming all initially issued restricted stock awards to management and employees are vested, accounting for 10% ownership, with the remaining 0.6% owned by certain equity investors. As a result, BRC would have an 89.4% claim on the residual value of BRS’ operating business, along with cash and investments held at the entity. As of Sept. 30, 2025, BRS had cash of $61.1 million and securities owned at fair value of $84.8 million. The company did not disclose cash and investments as of Dec. 31, 2025. BRS held 15.6 million shares of B&W as of March 31, worth approximately $271.6 million as of April 10.

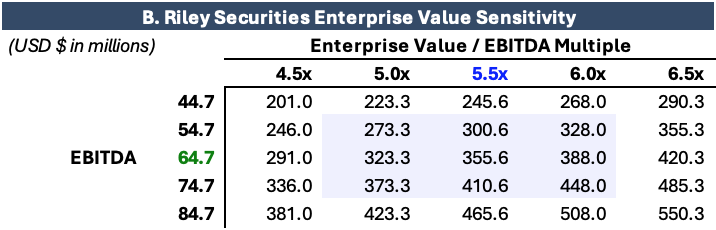

Candid Value estimates BRS’ enterprise value at $275 million to $450 million on the basis of normalized operating adjusted EBITDA of about $65 million and enterprise-value-to-EBITDA multiples in a range of 4.5x to 6.5x. BRS’ enterprise value is sensitized at a broader array of normalized earnings power and EV/EBITDA multiples below.

Publicly traded “elite” boutique banks, including Evercore, Lazard, PJT, Moelis and Perrella Weinberg, trade at an EV-to-operating-adjusted-EBITDA range of 9x to 13x, based on Candid Value’s estimates.

Candid Value believes that BRS should trade at a lower multiple than its “elite” boutique peers because of its riskier mandates, smaller client size and recent underperformance characterized by declining year-over-year sales and EBITDA, contrary to the broader investment banking sector which has experienced a pickup in deal flow. Candid Value maintains that BRS’ underperformance, significant reputational harm tied to FRG and Kahn, and delays in SEC filings warrant a risk-adjusted haircut to its valuation multiple. We believe an EV/EBITDA multiple range of 4.5x to 6.5x is more acceptable for BRS.

Candid Value uses historical financials for BRC’s capital markets segment as a proxy for BRS’ normalized business operations. We calculate normalized revenue on the basis of averages for 2022, 2023 and 2024, excluding the second and third quarter of 2024 because of underperformance. Employee compensation and benefits are held at 62% as a percentage of services and fee revenue, in line with 2023. Additional operating expenses are estimated based on the LTM period ended Sept. 30, 2025, amounts or margins, as shown below. Candid Value adds back stock-based compensation estimated based on BRS’ average reported for the second and third quarters of 2025. We allocate $15.5 million of BRC’s consolidated corporate expenses of $56.1 million for the LTM period ended Sept. 30, 2025, to BRS.

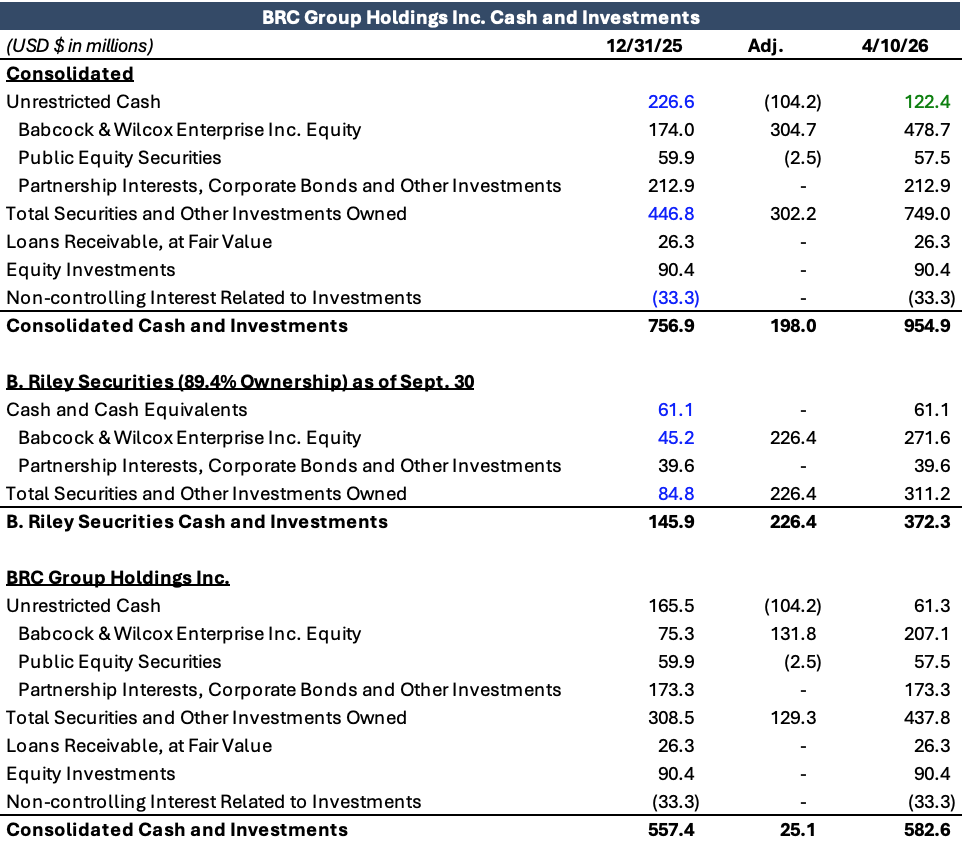

Consolidated BRC Cash and Investment Estimated at $955M as of April 10

Candid Value estimates that consolidated cash and investments for the entire BRC structure could total approximately $954.9 million based on fair value for investments as of Dec. 31, 2025, and the market value of certain specifically disclosed equity investments as of April 10, assuming BRC still holds these investments after Dec. 31, 2025.

As of March 31, BRC owns 27.5 million total shares of B&W, which we value at $478.7 million based on a $17.44 price per share as of April 10. According to B&W’s schedule 13D filed Feb. 13, B. Riley Securities Inc. holds 15.6 million B&W shares and BRF Investments LLC holds 11.9 million B&W shares as of Dec. 31, 2025.

For valuation purposes, Candid Value assumes that 89.4% of the cash and investments held at BRS, particularly its 15.6 million shares of B&W, would be attributable to the BRC structure as noted above.

While the company includes amounts due from clearing brokers and securities sold and not yet purchased in its investment value calculation, Candid Value omits these amounts so as to not double-count or inflate the implied value of BRC’s institutional brokerage business already embedded in BRS’ normalized operating adjusted EBITDA.

Cash and investments values as of Dec. 31, 2025, versus current equity market values and pro forma cash balances held at various silos are shown below.

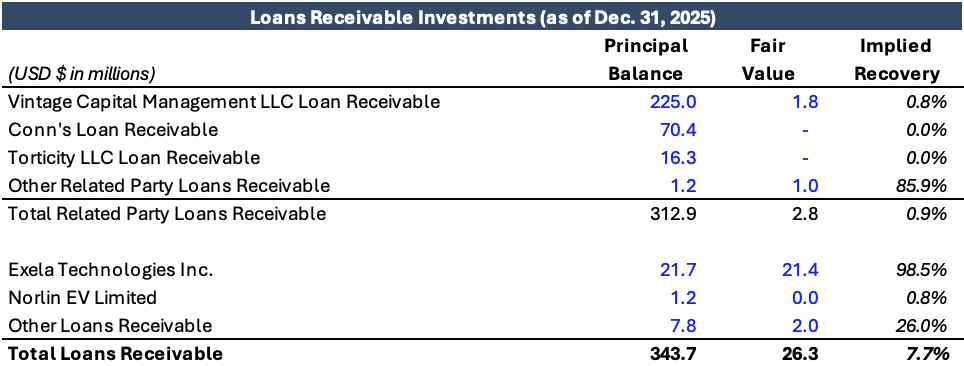

As of Dec. 31, 2025, loans receivable totaled $26.3 million at fair value and $343.7 million in principal balance, “net of discounts,” as shown below.

Equity method investments totaled $90.4 million as of Dec. 31, 2025, as shown below.

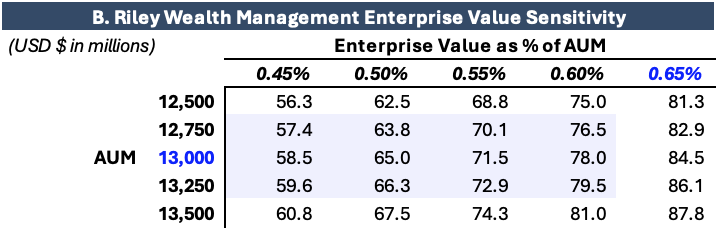

Wealth Management Enterprise Value Estimated at $60M to $80M at a Haircut to Stifel Sale

Candid Value values BRC’s wealth management segment in a range of $60 million to $80 million, based on $13 billion of AUM as of Dec. 31, 2025, and an EV as a percentage of AUM range of 0.45% to 0.6%. This range is a haircut to BRC’s recent sale of part of its wealth management business at a sale price of approximately 0.65% of AUM.

On April 4, 2025, the company sold a portion of its W-2 wealth management business, including 36 financial advisors whose managed accounts represented approximately $4 billion of total AUM as of the close of the sale, to Stifel for net cash consideration of $26 million. BRC had 231 financial advisors remaining as of the close of that sale, however the company has mentioned the loss of additional financial advisors over the last several quarters. Total AUM under this segment has decreased to approximately $13 billion as of Dec. 31, 2025, compared with AUM of $18.4 billion as of March 31, 2025, immediately prior to the sale.

While looking at precedent transactions in the wealth management sector, Candid Value observed a wide range of sale considerations as a percentage of AUM. We chose not to use EV/EBITDA as a valuation method because it was difficult to decipher normalized EBITDA for the remaining business, which has generated negative EBITDA since the sale. The company has not yet provided adjusted or restated historical financials for the remaining business.

BRC has noted a 60%/40% split in the count between independent contractor 1099 financial advisors and company-employed W-2 financial advisors, dating back to Sept. 30, 2023. Industry sentiment dictates that W-2 wealth management businesses generally trade at a higher multiple than 1099 wealth management businesses because of the stickiness of advisors and ownership of client relationships. The current head count and financial splits of BRC’s wealth management division are not disclosed, making it complicated to value the company’s 1099 business and remaining portion of its W-2 business at different valuations.

As a result, Candid Value applies a haircut to its Stifel sale price as an AUM percentage of approximately 0.65%, aiming to incorporate a lower multiple afforded to its 1099 business. BRC’s wealth management enterprise value is sensitized at varying AUMs and valuation percentages below.

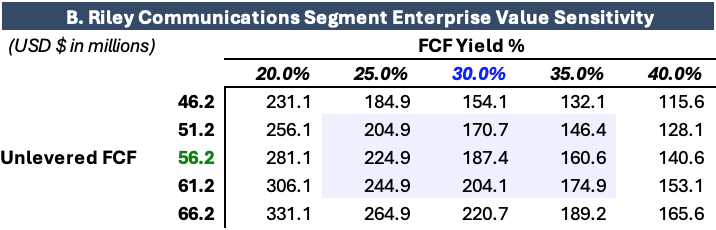

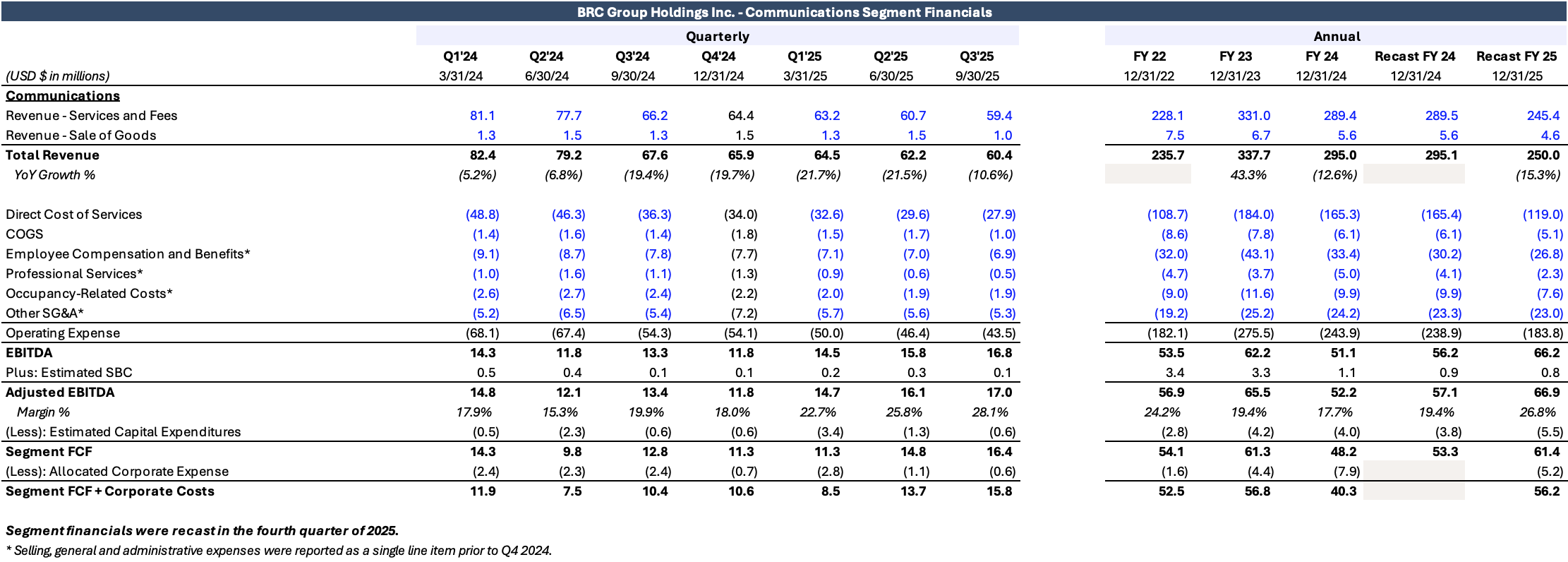

Communications Segment Enterprise Value Estimated at $145M to $245M, Facing High Secular Headwinds

Candid Value approximates the enterprise value for BRC’s communications segment at $145 million to $245 million on the basis of recent annual unlevered free cash flow of $50 million to $60 million and a FCF yield of 25% to 35%. Although the segment continues to generate a significant portion of BRC’s FCF, we believe that the business faces severe secular headwinds surrounding landline and voice over internet protocol technology obsolescence. As a result, we use a high FCF yield hurdle for the communications business.

This segment generated $56.2 million and $40.3 million of unlevered FCF before working capital in 2025 and 2024, respectively, based on Candid Value’s estimates for stock-based compensation and capital expenditures and including an allocated portion of corporate expenses. The company does not provide details surrounding working capital inflows and outflows, making it difficult to estimate them for the segment. Historical FCF estimates for the communications segment are shown below.

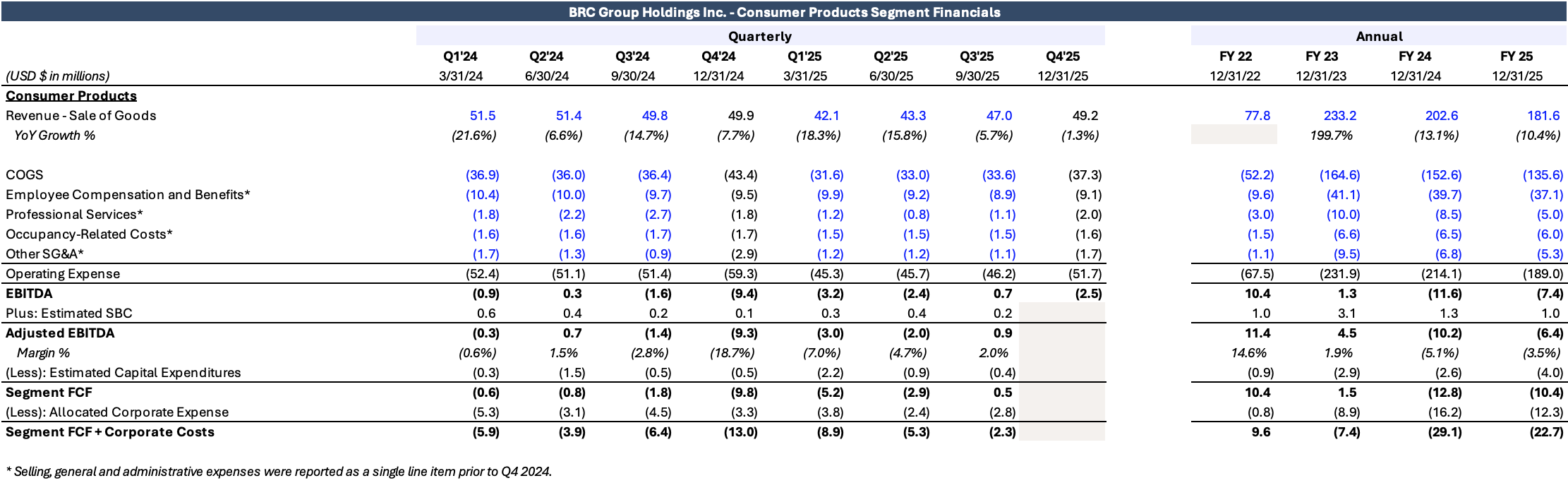

Targus Enterprise Value Likely De Minimis as FCF Burn Continues

Candid Value ascribes no distributable value to BRC’s consumer products segment, which comprises the computer accessories brand Targus. Targus continues to experience year-over-year revenue declines and generate negative EBITDA. According to the 2025 10-K, Targus’ accounts receivable and inventory have collateral value, as defined under its revolving credit facility credit agreement, of $34 million and $44.8 million, respectively, as of Dec. 31, 2025.

Targus generated negative $22.7 million and negative $29.1 million of unlevered FCF before working capital in 2025 and 2024, respectively, based on Candid Value’s estimates for stock-based compensation and capital expenditures and including an allocated portion of corporate expenses. Historical FCF estimates for Targus are shown below.

bebe Stores Inc. Value Likely De Minimis as Comparable Buddy’s Furnishings Franchisees Struggle

The “all other” segment of BRC seems to predominantly house the company’s 76.2% ownership of bebe Stores Inc., pro forma the sale of Atlantic Coast Recycling on March 3, 2025. bebe Stores Inc. shifted its strategy from an apparel clothing brand to a holding company model in 2020, and it now owns and operates over 60 Buddy’s Home Furnishings stores as their franchisee. While the company does not explicitly report bebe Store Inc.’s earnings, we suspects that the “all other” segment’s financials for only the second and third quarters of 2025 illustrate the franchisee’s earnings. The company combined the reporting of its “all other” segment with its corporate segment in the fourth quarter of 2025.

Candid Value ascribes no value to bebe Store Inc. In comparison, a similar franchisee of Buddy’s Home Furnishings named Buddy Mac filed for chapter 11 on Dec. 1, 2025.