QVC: Long 6.375% Notes Due 2067 / 6.25% Notes Due 2068

Long 6.375% QVC Inc. Notes Due 2067 at ~10.91 / 6.25% QVC Inc. Notes Due 2068 at ~10.84 as of Sept. 23, 2025

〰️

Long 6.375% QVC Inc. Notes Due 2067 at ~10.91 / 6.25% QVC Inc. Notes Due 2068 at ~10.84 as of Sept. 23, 2025 〰️

Situation Overview

Home television shopping network and video commerce retailer QVC Group Inc. (NASDAQ: QVCGA) is experiencing accelerated volume declines amid deteriorating consumer sentiment tied to global economic uncertainty and the knock-on effects of tariffs. While cord-cutting has been a looming secular headwind for over a decade, recent events indicate that the structure may have finally reached its breaking point.

“Less than half” of QVC’s domestic business (QxH) product is sourced from China. Management previously stated that QxH would not feel the impact of tariffs until the second half of the year, having benefited from prior inventory build. Yet, the company has significantly underperformed in the first half of the year with revenue down 8.6% year over year and adjusted OIBDA down 24.4% year over year compared with the prior-year period. QVC’s recent underperformance is increasingly concerning since tariffs have not yet hit the income statement and they would only exacerbate the situation. However, the temporary “truce” between the U.S. and China, which reduced U.S. tariffs on Chinese goods to 10% until Nov. 10, could provide the company with some breathing room.

QVC’s customer churn has significantly accelerated this year with QxH customers decreasing to 7.2 million for the trailing-twelve-month period ended June 30, compared with 7.9 million customers in the prior-year period, 8.1 million in 2023 and 8.9 million in 2022. In an attempt to offset cord-cutting, management implemented initiatives in November 2024 aimed at driving over $1.5 billion of run-rate revenue from social media and streaming platforms by 2027, while maintaining “stable” double-digit adjusted OIBDA margin (supported by a $100 million+ cost-savings program). The company also administered measures to reduce products sourced from overseas to less than one-third of total supply for any single country. The level of success of these initiatives would provide significant upside in all future restructuring scenarios.

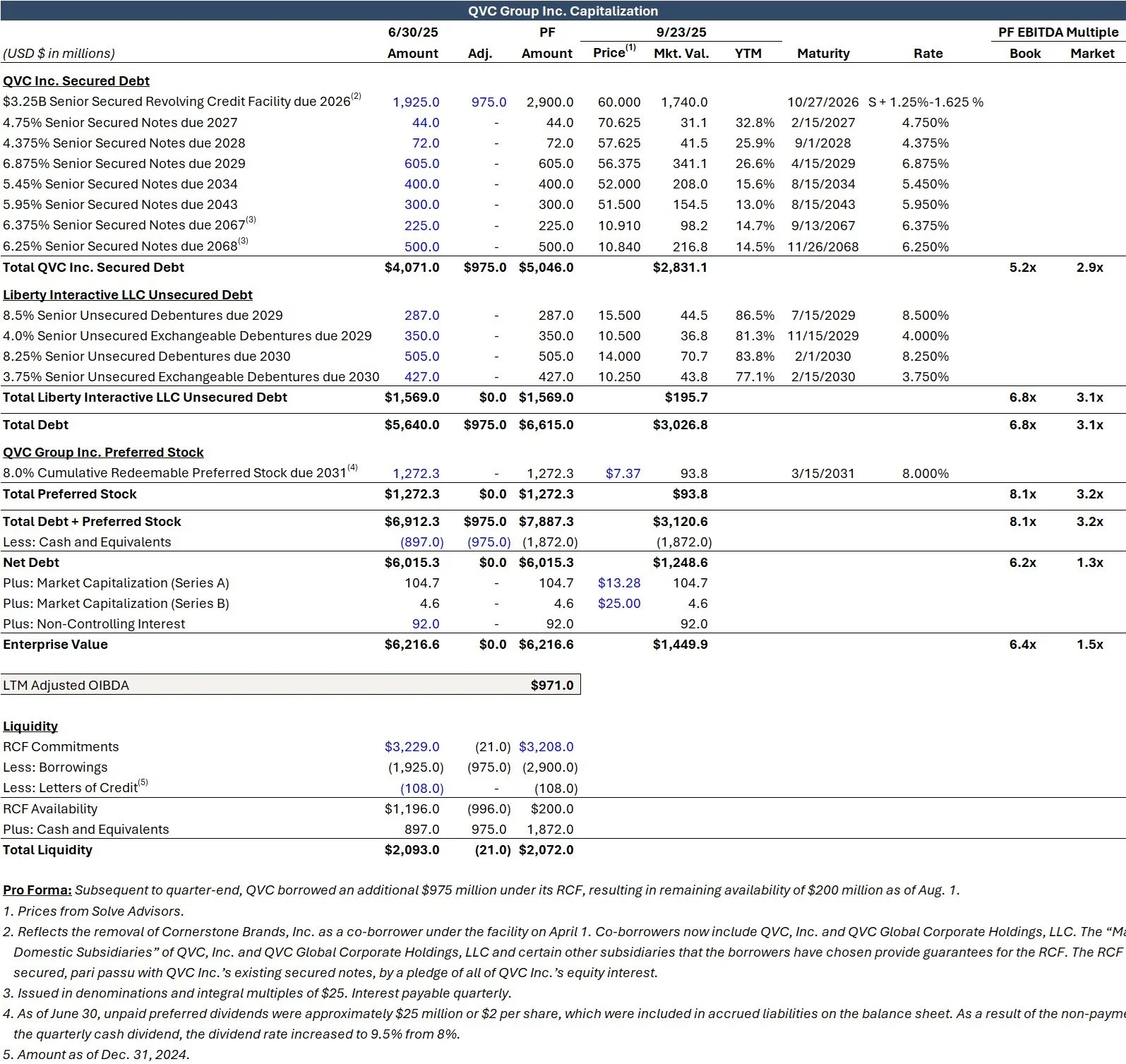

QVC Group Inc. has significant net leverage of 6.2x, compared with other retailers such as Macy’s (NYSE: M) of 0.9x and Kohl’s (NYSE: KSS) of 3.2x. As of June 30, the QVC structure had $5.6 billion of debt, consisting of $4.1 billion at OpCo QVC Inc. and $1.6 billion at HoldCo Liberty Interactive LLC, or LINTA, and $1.3 billion of preferred stock at ParentCo QVC Group Inc. Consolidated cash totaled $897 million, of which $330 million was at QVC Inc., $200 million at LINTA, $262 million at QVC Group Inc. and $105 million at Cornerstone Brands Inc. as of June 30.

On a consolidated basis, QVC has burned $156 million of free cash flow in the first half of 2025, compared with FCF generation of $164 million in the prior-year period. QVC’s liquidity continues to dwindle ahead of the maturity of its revolving credit facility on Oct. 27, 2026. The RCF is succeeded by a 2029 maturity wall and an estimated aggregate tax liability of $850 million owed at the maturity of the LINTA exchangeable debentures in 2029 and 2030. The LINTA exchangeable debentures allow for tax deductions at interest rates of 9.069% and 9.43%, in excess of their cash coupon rates of 4% and 3.75%, respectively, creating a current period cash tax benefit and a simultaneous contra deferred tax liability, which compounds until and is due at the maturity of each debenture.

Candid Value suspects that recent events at QVC point to a near- to medium-term restructuring. Subsequent to the end of the second quarter, QVC Inc. borrowed an additional $975 million on its RCF, increasing its balance to $2.9 billion (with remaining availability of $200 million as of Aug. 1), and increasing pro forma consolidated QVC Group Inc. cash to $1.9 billion. QVC Group Inc.’s maturity schedule is illustrated below:

Candid Value believes this maneuver provides the company with considerable negotiating leverage against the RCF lenders, who would not want their newly drawn par commitments to recover pari passu with QVC Inc.’s other debt in a bankruptcy scenario, which is trading at 52 cents or less on the dollar as of Sept. 23. The RCF has recently been quoted at 60 cents on the dollar, according to third-party sources, above the recent prices of other pari debt at QVC Inc., accounting for potential upside from restructuring scenarios.

In Candid Value’s view, QVC has successfully mitigated the RCF’s temporal seniority, forcing lenders to the table to negotiate an extension of commitments ahead of its maturity. As a result, a group of lenders holding more than 75% of QVC’s RCF have signed a cooperation agreement to negotiate as a bloc with the company, in preparation for a possible liability management exercise, or LME, The Wall Street Journal reported on Aug. 13.

On Aug. 15, QVC disclosed that nine senior executives, including CEO David Rawlinson and CFO Bill Wafford, would be prepaid 50% and 100% of their target variable compensation for 2025 and 2026, respectively, in cash to retain them through the end of 2026. Candid Value believes this is a clear indicator that a near- to medium-term restructuring is imminent.

There is market speculation that QVC may be planning an LME. Given the limited value available at QVC, a thorough analysis of all potential restructuring scenarios is crucial, as some creditors are likely to be excluded in a transaction.

OpCo QVC Inc. Debt Increased to $5B as of Aug. 1

QVC Group Inc.’s capital structure pro forma the RCF drawdown is shown below:

Investment Thesis

A near-to-mid-term in-court or out-of-court holistic restructuring is inevitable at QVC Group Inc. Current securities’ trading prices, along with recent business performance and prevailing capital structure dynamics, indicate that a par refinancing is not within QVC’s cards. Candid Value suspects that any out-of-court restructuring will be “aggressive” with value being taken away from non-participating creditors. Based on QVC’s current debt documents, the only possible option for a holistic out-of-court restructuring would require amendments to the underlying credit agreement and each QVC note indenture.

When analyzing all possible capital structure scenarios through a game theory lens, Candid Value believes the QVC “baby bonds” due 2067 and 2068 provide the largest price appreciation upside with limited downside risk owing to their current air-tight covenants language. The QVC notes due 2067 and 2068 are protected in highly aggressive LME and bankruptcy scenarios. We expect the QVC notes due 2067 and 2068 to continue to clip their relatively high coupons, compared with other QVC notes, of 6.375% and 6.25% (paid on a quarterly basis on March 15, June 15, September 15 and December 15 of each year), respectively, until the structure finally collapses.

The indentures of the QVC notes guard them against subordination vis-à-vis the RCF and all other QVC notes, and against lien stripping with respect to assets of QVC Inc. and its restricted subsidiaries, except in the case of amendments to the underlying indentures (which would require 66.67% supermajority participation under each series) or a drop-down transaction (which is currently limited to only $150 million of restricted payment capacity, insufficient for a viable deal). In addition, the language under the indentures requires the notes to “tag along” in any potential comprehensive uptiering transaction, so long as their current covenants aren’t amended, the likelihood of which is very low for the QVC notes due 2067 and 2068 since they are illiquid securities, broadly held by retail investors.

The QVC notes due 2067 and 2068 are also covered in bankruptcy scenarios since they are already trading at recovery prices of approximately 43.5% as of Sept. 23.

QVC Notes Due 2067, 2068 Are Risk Adverse in Feasible Game Theory Scenarios

The outcomes for QVC’s capital structure can be illustrated through a simplified game theory exercise, as shown below:

The first branch is contingent on whether the company can execute an amendment and extension for its RCF. In our opinion, if the company is unable to negotiate an amend and extend, it would not have enough cash to pay down the facility, likely resulting in a bankruptcy filing in 2026. In this scenario, the QVC notes due 2067 and 2068 would receive 4 quarterly coupon payments followed by recoveries at their current trading prices of approximately 43.5% as of Sept. 23.

On the other hand, a successful RCF amendment and extension could be executed in one of two ways – as part of a holistic restructuring of the QVC capital structure or on a stand-alone basis.

QVC Notes Due 2067, 2068 Would Likely ‘Tag Along’ in an Uptiering Scenario

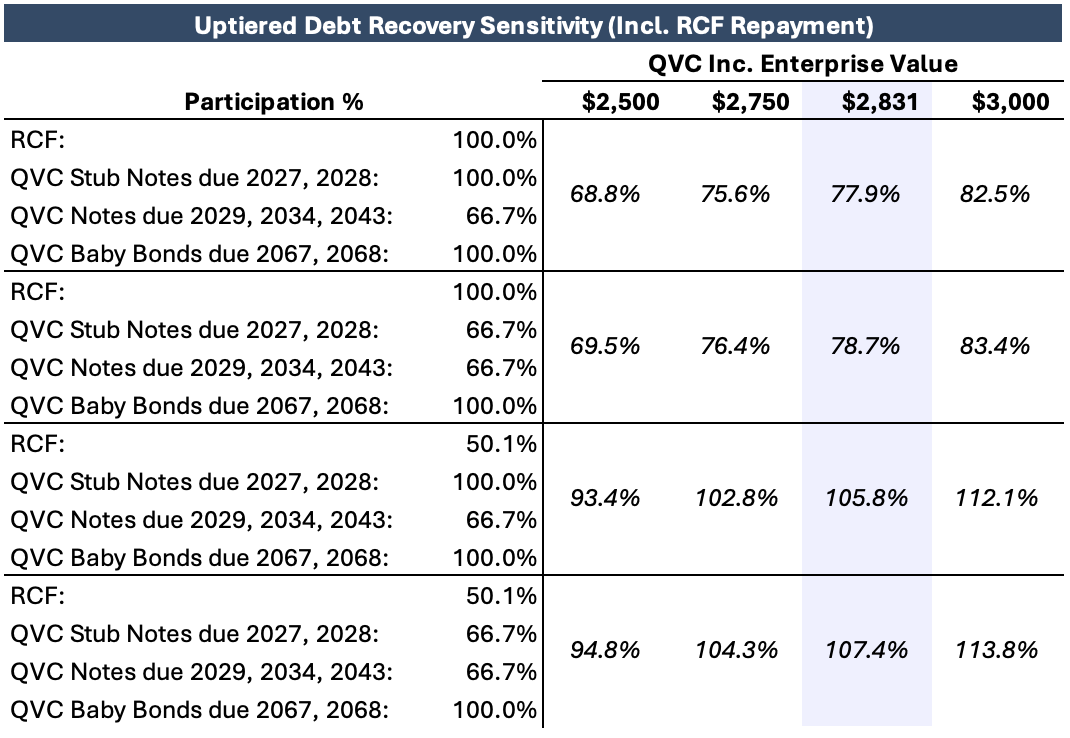

Although the current language under QVC’s credit agreement and indentures offers insufficient capacity to execute a holistic LME, a comprehensive restructuring could be achieved by amending each underlying debt document. This could be accomplished through (1) full 100% pro rata participation of the RCF lenders and at least 66.67% supermajority participation within each of the seven series of QVC notes, or (2) at least 50.1% majority non-pro-rata participation of the RCF lenders and the same at least 66.67% supermajority participation within each series of QVC notes. Albeit, a non-pro-rata uptier within the RCF involving less than 100% participation would be highly unprecedented. A deal might also include a partial RCF paydown or amortization schedule given the large lump sum recently borrowed under the RCF.

Candid Value believes a holistic restructuring could involve all or majority RCF lenders and supermajority QVC noteholders uptiering their claims through receipt of senior liens closer to, or explicitly on, QVC Inc.’s assets, a drop-down transaction or something along those lines. Given the number of debt securities at play, a deal of this magnitude could easily fall apart without the requisite consents.

The RCF and QVC notes are currently secured on a pari passu basis only by the capital stock of QVC Inc., via a stock pledge from the parent Qurate Retail Group Inc., but not directly against the assets at QVC Inc. and its subsidiaries. QVC Inc. could offer any lenders liens on these presently unencumbered assets of the QVC Inc. restricted group. However, any liens on QVC Inc. restricted group assets granted to the RCF or QVC notes would require using the pari liens basket under the QVC notes’ indentures, which permits up to $5 billion of liens on collateral assets of the restricted group to secure the RCF or other pari debt so long as the liens are shared equally and ratably with the notes. In other words, the lien sharing requirement prevents the RCF or any series of QVC notes from gaining an advantage over one another via effective subordination.

As a result, any non-amended indenture would retain language granting the underlying note pari liens on any additional credit support provided to an uptiered lender group. However, if the required supermajority participation is successfully achieved within the series, all nonparticipating lenders would effectively be subordinated.

Amendments to the QVC notes’ indentures are only possible through 66.67% supermajority consent under each series. The 6.375% secured notes due 2067 and 6.25% secured notes due 2068, commonly referred to as “baby bonds,” are issued in denominations of $25 and generally intended for retail investors. These securities are broadly held and illiquid meaning it would be extremely difficult to organize, or for a party to own a supermajority share within each series, to amend their underlying indentures. In an aggressive LME scenario, the QVC notes due 2067 and 2068 would preserve the language requiring any additional collateral provided to the RCF or any other QVC note to be shared equally and ratably with them, effectively “tagging along” in any LME.

In this scenario, recoveries for the QVC notes due 2067 and 2068 would depend on the estimated value of QVC Inc., which is approximately $2.8 billion based on implied market value as of Sept. 23, shared pari passu with other participating lenders. Additionally, the QVC notes due 2067 and 2068 would continue to receive their quarterly coupon payments. Recoveries for the uptiered lender group sensitized at varying participation levels and varying QVC Inc. enterprise values would be as follows:

Recoveries for uptiered lenders in the event that QVC repays the $975 million RCF drawdown are shown below:

Nevertheless, investors should keep an eye out for the potential formation of a supermajority group within their respective series. If a supermajority group is organized within their series, investors must join the group as to not be subordinated or have their liens stripped.

Stand-Alone RCF Amend & Extend Would Yield Additional Coupon Payments, Followed by a Comprehensive In-Court or Out-of-Court Restructuring

In the case of a stand-alone RCF amendment and extension, Candid Value expects that QVC Inc. would likely extend its RCF to 2029, ahead of the maturity of the 6.875% QVC notes on Apr. 15, 2029, potentially including a partial paydown or amortization schedule since there are limited options for adequate additional collateral support solely for the RCF. As discussed above, only providing RCF lenders with credit support from assets of the QVC Inc. restricted group without providing pari liens to QVC noteholders is not feasible under the current debt documents.

A successful extension of the RCF would allow the company time to implement its social media and streaming strategy and supply chain and cost initiatives as it would likely gear up for a more comprehensive refinancing or in-court or out-of-court restructuring ahead of its extended maturity wall in 2029. However, if current business trends persist, Candid Value suspects the extended maturity wall and LINTA exchangeable debentures’ deferred tax liability would likely be a catalyst for a bankruptcy filing in 2029, discussed in detail below.

Candid Value believes that if an amendment and extension of the RCF is not followed by a comprehensive restructuring, QVC would likely file for bankruptcy at the extended RCF maturity in 2029. In this scenario, the QVC notes due 2067 and 2068 would receive 12 quarterly coupon payments followed by recoveries close to their current trading prices of approximately 43.5% as of Sept. 23.

LINTA Deferred Tax Liability Is a Catalyst for Bankruptcy in 2029

Candid Value estimates that the deferred tax liability tied to the LINTA exchangeable debentures due 2029 and 2030 would balloon to approximately $1.7 billion at maturity, although QVC forecasts that deferred tax assets stemming from unused cash interest tax benefits in current and future years would offset approximately half of this, decreasing the ultimate tax claim to approximately $850 million. Importantly, the subsidiary, or credit box, ultimately liable for the claim is contingent on the intercompany tax sharing agreement, which does not appear to be publicly available.

The tax claim adds a layer of complexity to the entire QVC Group Inc. capital structure since it is unclear which credit box would be liable. Candid Value believes that the subsidiary liable for the tax liability would likely use the bankruptcy process to induce a haircut on the payment. The IRS has historically taken significant haircuts on tax liabilities in similar situations. For example, Endo International plc’s priority tax claim of $2.3 billion was ultimately settled with a one-time payment of $200 million on the effective date in full satisfaction of the claim.

Candid Value believes that in a bankruptcy context, the tax liability would be classified as an unsecured claim with the potential for some amount of it to be treated as a priority unsecured claim, ahead of the other unsecured debt at that entity. Section 507(a)(8) of the Bankruptcy Code provides priority treatment for income or gross receipts taxes “for which a return, if required, is last due, including extensions, after three years before the date of the filing of the petition.” This three-year lookback priority tax claim is junior to administrative expense claims (including professional fee claims and claims for providing postpetition goods or services to a debtor) but senior to general unsecured claims. Claims for taxes beyond the three-year window are treated as general unsecured claims, unless a tax lien has been filed – for the purposes of this analysis, we assume no tax liens have been filed to secure either priority or nonpriority tax claims.

Under section 1129(a)(9)(C) of the Bankruptcy Code, a plan of reorganization must provide for payment of section 507(a)(8) priority tax claims in regular cash payments over up to five years after the petition date that equal the value of the allowed amount of the claim as of the effective date.

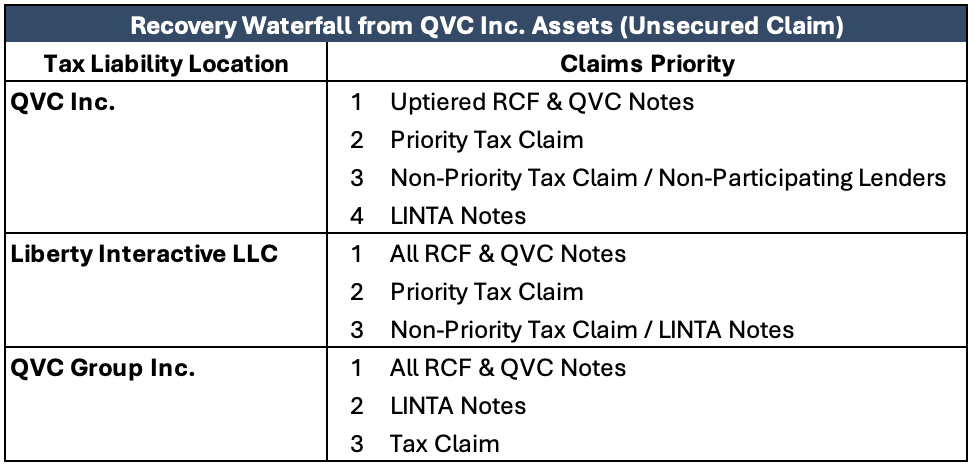

Current RCF, QVC Notes Should Be Treated as an Unsecured Claim in BK; Location of Tax Claim Would Affect Recoveries

Candid Value believes that as it stands right now, in a bankruptcy context, the RCF and QVC notes would be treated as an unsecured claim at the QVC Inc. level since they are only secured by a parent pledge agreement of the equity of QVC Inc., as illustrated in the organizational structure further below. However, because of that pledge agreement, the RCF and QVC notes are structurally senior to the LINTA notes with regard to the assets at QVC Inc. In a bankruptcy scenario where all credit boxes file, Candid Value anticipates the recoveries from QVC Inc.’s assets would be dependent upon the location of the unsecured tax claim, as illustrated below:

However, if the aforementioned uptiering scenario occurs, lenders awarded senior liens on QVC Inc.’s assets would become senior to priority and non-priority unsecured claims, or non-participating lenders. The QVC notes due 2067 and 2068, which would have been uptiered, would now recover on QVC Inc.’s assets based on the location of the tax claim as shown below:

Candid Value assumes that the IRS would not “nuke” a pre-packaged bankruptcy plan by asserting the full tax claim. Uptiered RCF and QVC notes would be senior to the unsecured tax claim, otherwise, in a scenario where no uptiering occurs, Candid Value suspects the QVC notes due 2067 and 2068 are already trading at recovery prices, limiting their downside.

An Aggressive LME Could Solve QVC’s Capital Structure Problems

Candid Value believes that the company would most likely file for bankruptcy in 2029 in order to deal with the maturity wall or LINTA deferred tax liability, or as a mechanism to crystalize an aggressive LME. QVC’s social media and streaming initiatives would serve as a caveat against filing, if the strategy gains enough traction to offset QVC’s steep volume declines and return the company to growth.

However, if current business trends persist, Candid Value believes that the company could deploy the following aggressive tactics to remedy its liquidity, 2029 maturity wall and deferred tax liability, all while deleveraging its capital structure:

The aforementioned holistic restructuring, which would result in all or majority RCF lenders and supermajority QVC noteholders uptiering their claims (while extending RCF commitments to 2029);

Followed by QVC Inc. and Liberty Interactive LLC filing for bankruptcy in 2029, which would result in:

Uptiered RCF lenders and QVC noteholders receiving senior secured takeback paper and potentially a portion of post-reorg equity;

Subordinated RCF lenders and QVC noteholders being equitized and receiving a portion of post-reorg equity;

QVC Inc. or LINTA (whoever is liable for the deferred tax liability) paying the tax claim at a significant haircut; and

LINTA noteholders receiving recoveries based on the assets listed below.

Even in this aggressive LME scenario, the QVC notes due 2067 and 2068 would share in capturing all remaining value left at QVC Inc. through takeback paper and potentially post-reorganized equity.

Appendix

Three Credit Boxes at QVC; OpCo Has Historically Sent Cash Up to TopCos

The majority of the value within the QVC Group Inc. structure is ascribed to and generated by OpCo QVC Inc. The OpCo has historically funded the bulk of the cash needs for TopCo entities LINTA and QVC Group Inc., including interest/dividend, principal and tax payments. A simplified organizational structure is shown below:

There are no cross guarantees or cross defaults among credit boxes within the QVC Group structure. QVC Inc. debt does not have cross-default provisions to the LINTA notes. Cross-default under the QVC credit agreement is triggered only by a default under "Material Indebtedness," the definition of which is limited to debt of the borrower and its restricted subsidiaries. Because the LINTA notes sit above QVC Inc. and are not guaranteed by QVC Inc., they are not debt of the restricted group. The QVC secured notes likewise do not cross-default to the LINTA notes for similar reasons.

As of June 30, assets at LINTA comprised $200 million of cash; 100% of the pass-through equity interest of QVC Inc., which value is likely de minimis; 38% equity interest of Cornerstone Brands Inc., which value is highly impaired due to its recent performance, although the subsidiary holds $105 million of cash; 80% ownership in Liberty Technology Venture Capital II LLC and varying noncontrolling ownership interests in the LIC Sound LLC portfolio of assets. In 2017, the company valued its Liberty Venture assets at $75 million, but no fair value estimate has been recently provided. LINTA has a $1.74 billion promissory note issued to QVC Global Corporate Holdings LLC as of June 30, which has a stated interest rate of 0.48% and a maturity of Dec. 29, 2029. The seniority of the note and whether it is secured or unsecured is unknown.

Assets at QVC Group Inc. consist of the following: $262 million of cash as of June 30; 100% equity interest of Liberty Interactive LLC, which is likely de minimis due to significant debt and limited value at the subsidiary; and 62% equity interest of Cornerstone Brands Inc, which holds $105 million of cash as discussed above.

FCF Burn Has Accelerated Ahead of the RCF Maturity

FCF burn on a consolidated basis for QVC Group Inc. was $8 million in the second quarter, compared with FCF generation of $191 million in the prior-year period. Consolidated FCF for QVC Group Inc. is illustrated below:

FCF for OpCo QVC Inc. before dividends to TopCo entities was negative $37 million in the second quarter, compared with positive $93 million in the prior-year period, as shown below: